Minneapolis and neighboring St. Paul show many signs of a strong recovery from the recent economic downturn. Healthcare, finance, and consumer goods companies are thriving in the Twin Cities. Nineteen Fortune 500 companies are based in the metro area, seven of which appear on Forbes’ 2012 list of largest private companies. Area universities provide the market with an educated workforce, and with a student body of more than 50,000, the University of Minnesota boasts one of the largest enrollments in the U.S. Recent accolades from major organizations and publications speak to Minneapolis’ high quality of life, and a thriving arts and dining scene placed Minneapolis on Travel + Leisure’s list of “Hottest Travel Destinations” for 2013. Together, these attributes make Minneapolis a powerfully attractive destination for leisure, commercial, and meeting and group travelers.

Economy Update

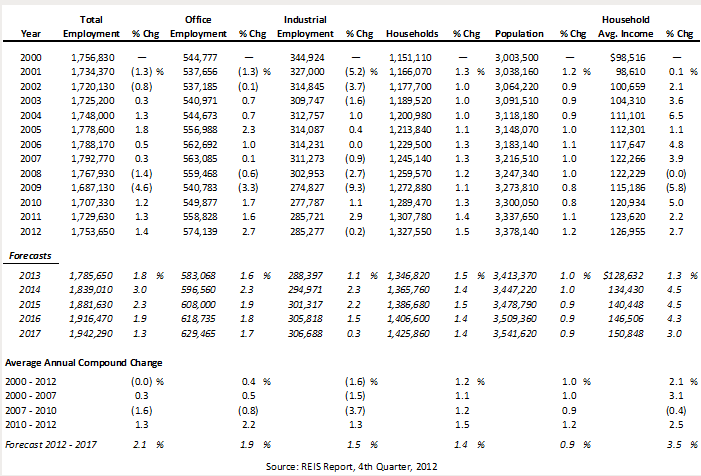

The following table illustrates historical and projected employment, population, and income data for the overall Minneapolis market.

HISTORICAL & PROJECTED EMPLOYMENT, HOUSEHOLDS, POPULATION, AND HOUSEHOLD INCOME STATISTICS

Of the roughly 1.8 million persons employed in Minneapolis, 33% are categorized as office employees and 16% as industrial employees. Total employment decreased by an average annual compound rate of -1.6% during the recession of 2007 to 2010, followed by an improvement of 1.3% from 2010 to 2012. By comparison, office employment reflected compound change rates of -0.8% and 2.2% during the same respective periods. Total employment is anticipated to expand by 1.8%, and office employment by 1.6%, in 2013. Total employment is expected to improve at an average annual compound rate of 2.1% for the period of 2012 through 2017, and office employment is forecast to improve by 1.9% on average annually during the same time frame. Household average income is forecast to grow by an average of 3.5% annually between 2012 and 2017.

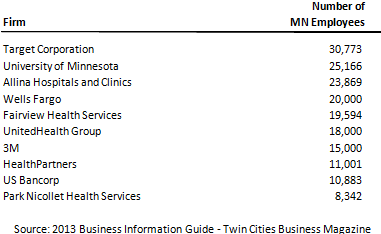

The following table highlights major employers with operations based in the Minneapolis-St. Paul metropolitan area.

MAJOR EMPLOYERS

The healthcare sector is heavily represented in the list above, and the metro area is also home to high-profile companies such as Cargill, Best Buy, General Mills, and Target, the area’s largest employer. SuperValu announced that approximately 600 Eden Prairie-based employees would be laid off later this year, and Best Buy will be laying off 400 employees in the Minneapolis suburb of Richfield. Nevertheless, growth is occurring at other local companies, including UnitedHealth Group and General Mills, and the relocations of Pinnacle Airlines and other new companies to the local market are anticipated to offset some of these job losses.

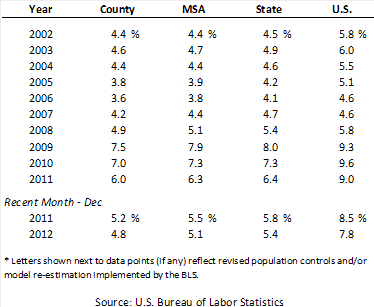

The following table lists unemployment figures in the greater Minneapolis area, as well as the state and nation as a whole, from 2002 to 2011.

UNEMPLOYMENT STATISTICS

Unemployment in Minneapolis remains well below the national level, a fact attributable to the city’s diverse economic base, which ranges from healthcare to banking to manufacturing. Unemployment increased in 2008 and more dramatically in 2009, a result of the recent recession; however, rates for 2010 and 2011 illustrate an improving trend. Data from the most recent comparative period reflect a continuing decline in unemployment.

Office Space Market Update

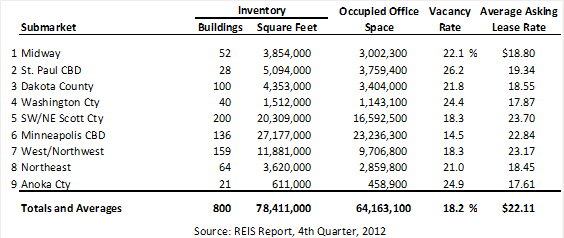

The following table details the Minneapolis-St. Paul area’s office space statistics, which are important indicators of a market’s propensity to attract commercial hotel demand.

OFFICE SPACE STATISTICS – MARKET OVERVIEW

Of the greater area’s more than 78 million square feet of office space, the Minneapolis CBD houses the largest inventory with the lowest vacancy rate and commands the second-highest average asking lease rate; the Southwest Minneapolis/NE Scott County submarket boasts the highest lease rate. With CBD parking rates reportedly above the national average, suburban areas like Brooklyn Park and Minnetonka are becoming popular locales for corporate expansions.

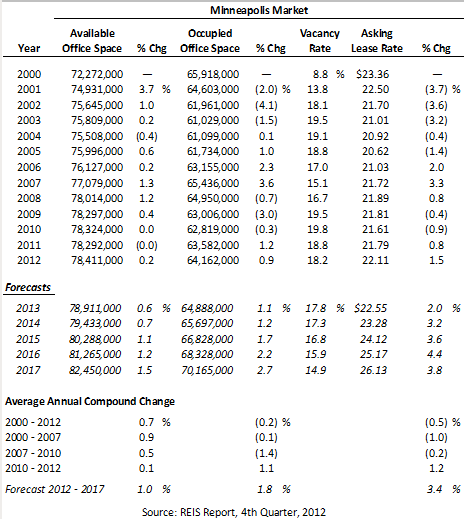

The following table illustrates historical and projected trends for office space statistics for the overall Minneapolis-St. Paul market.

HISTORICAL AND PROJECTED OFFICE SPACE STATISTICS – GREATER MARKET

The inventory of office space in the Minneapolis market increased at an average annual compound rate of 0.7% from 2000 through 2012, while occupied office space contracted at an average annual rate of -0.2% over the same period. The onset of the recovery is evident in the 1.1% average annual change in occupied office space from 2010 to 2012. From 2012 through 2017, the inventory of occupied office space is forecast to increase at an average annual compound rate of 1.8%. Available office space is expected to increase by 1.0%, resulting in an anticipated vacancy rate of 14.9% as of 2017, the lowest level realized since 2001.

Major developments in Minneapolis include the new Green Line light rail, which will connect Minneapolis and the University of Minnesota campus with Downtown St. Paul; the new line is scheduled to open in 2014. In addition, Vikings Stadium will be demolished and rebuilt in the Downtown East neighborhood; the Vikings are scheduled to play in the current stadium through 2013. The ease in metro travel, in addition to the upgraded sports facility, is expected to boost visitation to the greater metro area.

Hotel Construction Update

The 500-room Radisson Blu opened on March 15, 2013, on the south end of the Mall of America (MOA). This is expected to be the last large hotel to enter the market until the potential opening of a Downtown convention hotel, which is currently being evaluated. Additional hotels are planned in Bloomington, including an upscale hotel at Bloomington Central Station and a full-service hotel as part of Phase II of the MOA expansion. Smaller hotels are also proposed in Bloomington, Minnetonka, and Downtown Minneapolis, including a boutique hotel on 1st Avenue. While several new hotels are expected to enter the market in the coming years, the percentage increase to the overall market supply will be minimal.

Outlook on Market Occupancy and Average Rate

Occupancy remained relatively stable between 2011 and 2012 in the metro area, and average rate grew by approximately 3%. The growth in rate resulted in a RevPAR level comparable to that realized between 2007 and 2008, indicating that a market recovery is taking hold. Based on group bookings, year-to-date travel trends, and changes in supply, HVS anticipates that market occupancy will be relatively flat in 2013, followed by slight increases in 2014, 2015, and 2016 to a stabilized level of 63%. Given strong mid-week demand throughout the year, strong weekend demand during the summer months, and the entrance of some new upscale supply, average rate growth for the metro area is expected to rise above inflationary levels for the next several years.

Recent Hotel Transactions

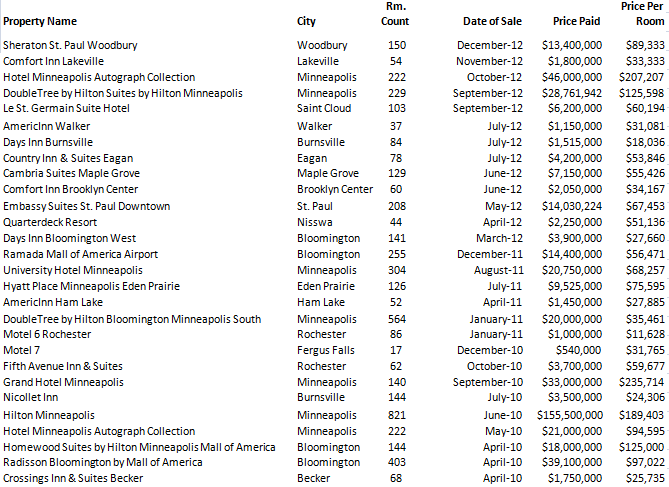

The following table lists hotel transactions in Minnesota from April of 2010 through December of 2012.

REVIEW OF HOTEL TRANSACTIONS

In addition to the sales listed above, the Crowne Plaza and DoubleTree in St. Paul were purchased for an undisclosed amount in March of 2013 by the Mille Lacs Band of Ojibwe. The former Comfort Suites in Downtown Minneapolis was purchased in October of 2012 for an undisclosed amount by an affiliate of Hyatt Hotels; this property is scheduled for renovation and conversion to a Hyatt Place by the summer of 2013, at which time Summit Hotel Properties will acquire the asset. The recent sales of the Comfort Suites and the Hotel Minneapolis Autograph Collection indicate the attractiveness of the market for institutional investors. Another Downtown property, the Hotel Ivy, is actively being marketed for sale.

Brokers convey confidence in Minneapolis’ hotel market given the diversity of the area’s economy and the quick recovery of occupancy following the recession, as well as a highly educated workforce and low unemployment levels in the city.

Conclusion

Expansions at local corporations and a drop in office vacancy to levels below those of 2005 both bode well for the continued economic growth in the greater Minneapolis market. Market-wide occupancy has shown stability in the last calendar year, and average rate growth has surpassed inflationary levels for the last two years. Given current demand trends and anticipated supply additions in the market, average rate is anticipated to surpass pre-recessionary levels in 2013. Together, these developments and forecasts provide for an optimistic outlook for the Minneapolis hotel market in the near term.