The survey discusses COVID-19 pandemic and its unprecedented impact on the Drive-In Hotel Markets. On a property level, the survey focuses on hoteliers’ point of view on reopening strategies, domestic demand profile, and market outlook. The survey discusses COVID-19 pandemic and its unprecedented impact on the Drive-In Hotel Markets. On a property level, the survey focuses on hoteliers’ point of view on reopening strategies, domestic demand profile, and market outlook. The survey was distributed to participants on 11 June 2020. The data collection period was available through 8 July 2020.

Survey Overview:

Re-Opening Strategy

- The level of effectiveness for each re-opening strategy measure

- Rooms Department

- Food & Beverage Department

- Marketing Department

- Others

- The implementation of guestroom promotions and packages

- The range of discount on the following offers:

- Guestrooms

- Restaurants

- Bars

- Spas

- Meeting Space

Demand Profile

- COVID-19 domestic market share

- Average length of stay and booking lead time

Market Outlook

- Domestic market’s recovery period

- International market’s recovery period

- Estimated and expected occupancy for 2020

- The market’s dynamic between pre- and post-COVID-19

Key Takeaways

- On 1st June 2020, the Thailand’s government eased the restrictions including the lifting of curfews, reopening of more businesses and activities, and allowing for cross provinces travel.

- Around 80% of the hotels that are currently in operation have re-opened their hotels to accommodate domestic demand.

- Once re-opened, hoteliers should communicate with prospective guests in case of any closure of facilities prior to confirming the reservation.

- Most hoteliers agree that staff training, social distancing, wearing masks, temperature checking, and SHA certificate are the most important measures to implement.

- Hoteliers are now active in marketing, which focus mainly on raising awareness of their properties, as well as increasing booking via a direct channel.

- Majority of responses are giving from 20% to more than 25% discount on guestrooms.

- Domestic leisure demand is expected to be the first market to recover in the short to medium term, followed by domestic corporate demand, while international demand would take more than one year to recover.

- Most hoteliers agree that the market will lure more domestic demand and that the hotels will employ less full-time staffs to be cost-efficient.

- The majority of respondents believes that the occupancy will reach at least 45% and up to over 75% by Q4 2020.

Respondents

Respondents by Hotel Positionings

Source: HVS

The majority of hotels in the sample survey are branded hotels. Approximately 35% of the properties in the survey sample are in the upper-upscale and upscale tiers.

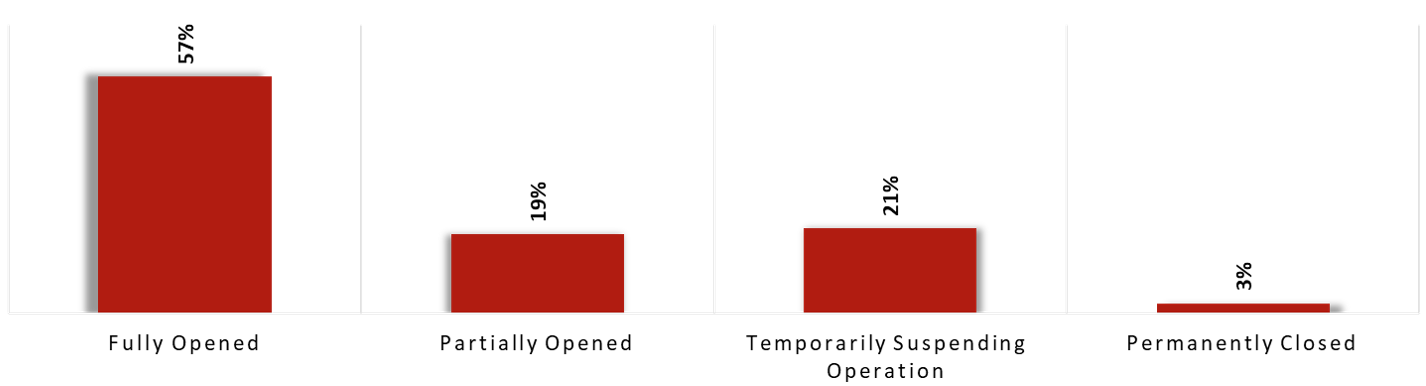

Respondents by its Opening Status

Source: HVS

More than 50% of the survey sample are fully opened for operations. 80% of the properties that are fully opened had suspended their operation for two months between April and May.

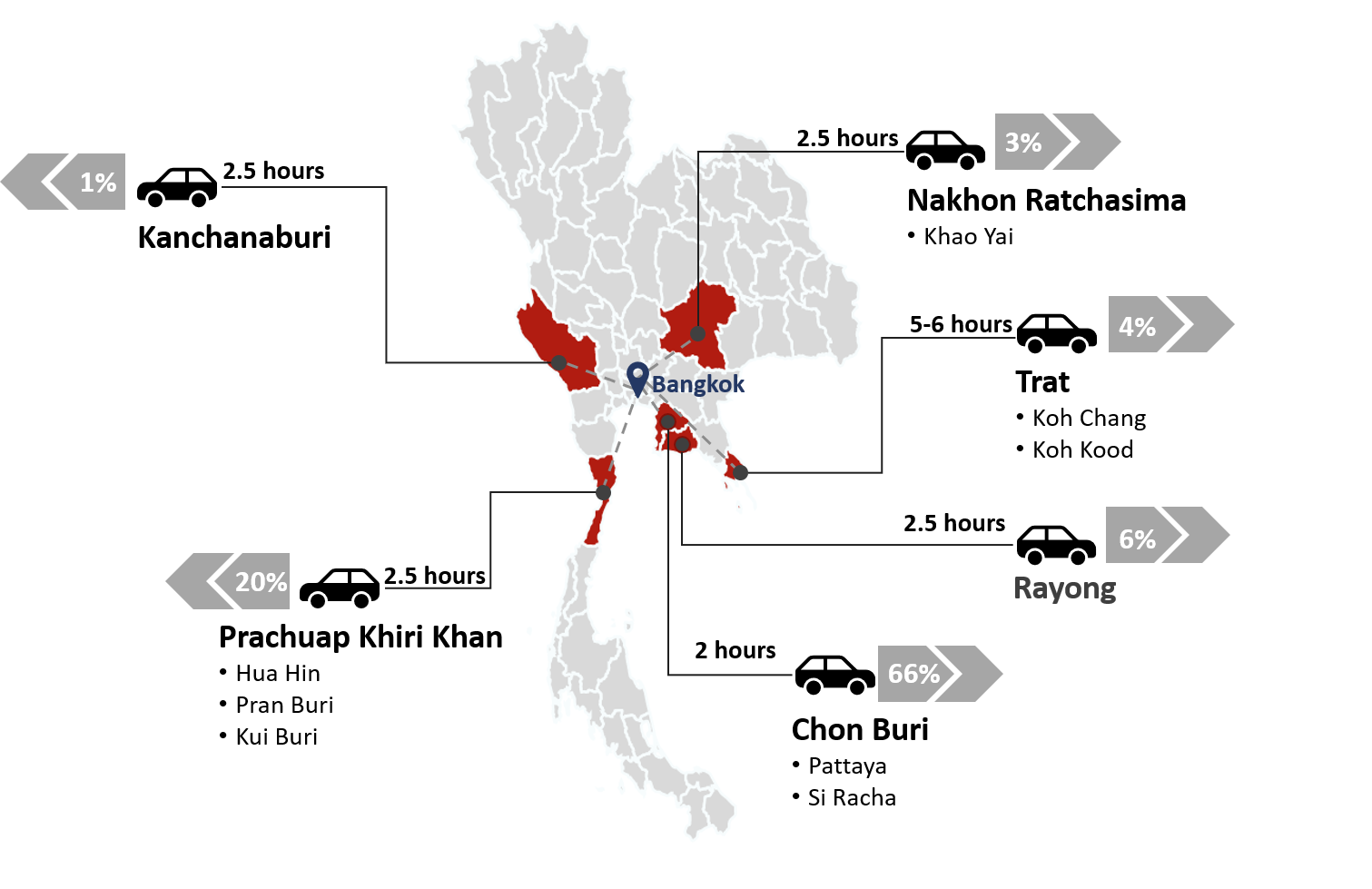

Respondents by Drive-In Destinations

Source: HVS

There are nine markets and six provinces within the survey.

Re-Opening Strategies

Rooms Department

What is the level of effectiveness for each measures?

Source: HVS

As some of the hotels from the sample only recently re-opened, some of the measures are not fully implemented. It is evident that the implementation of a new cleaning guideline is expected to be one of the most effective measures. The upfront cost for developing a mobile check-in platform is costly. Thus, using mobile check-in and check-out to reduce human contact is expected to be ineffective. The majority of the hotels have not implemented the system yet. Reducing daily housekeeping service received mixed comments as some argue that there is a demand for more cleaning to keep the hygiene of the rooms. In contrast, others prefer less housekeeping service to minimize human touch.

Food & Beverage Department

What is the level of effectiveness for each measures?

Source: HVS

46% of hotels in the survey sample have less than 100 rooms. Thus, these hotels offer limited food and beverage facilities and may not necessarily need to reduce F&B outlets. Disinfecting every table turnover is expected to be the most effective. Limiting capacity in food and beverage outlets is also deemed to be effective. Demand for in-room dining service is expected to become more prevalent in hotels to avoid crowded space. One of the new ways to operate the buffet is by letting the hotel staffs serve the food from a buffet line in order to avoid human touch with shareable items.

Sales & Marketing

What is the level of effectiveness for each measures?

Source: HVS

It is expected that raising awareness about safety and hygiene, as well as the hotel’s brand awareness, are deemed to be the most effective methods of marketing. Hoteliers are active in marketing, especially during COVID-19 pandemic, to reflect their commitments to support medical staffs and at the same time increase publicity. Hoteliers rather focus on direct booking instead of increase booking via OTAs channel. It is a good opportunity for hotels to increase their bookings via the direct channel.

Others

What is the level of effectiveness for each measures?

Source: HVS

Most hoteliers agree that applying social distancing policy, limiting capacity, and partnering with professional cleaning companies would be effective for hotels’ facilities and public spaces. The hotels are encouraged to deliver clear messages to guests should there be any changes in the hotel’s facilities or public space policy prior to confirming the booking reservation. Partnering with the cleaning company is expected to take time as the decision is generally being made from a corporate level.

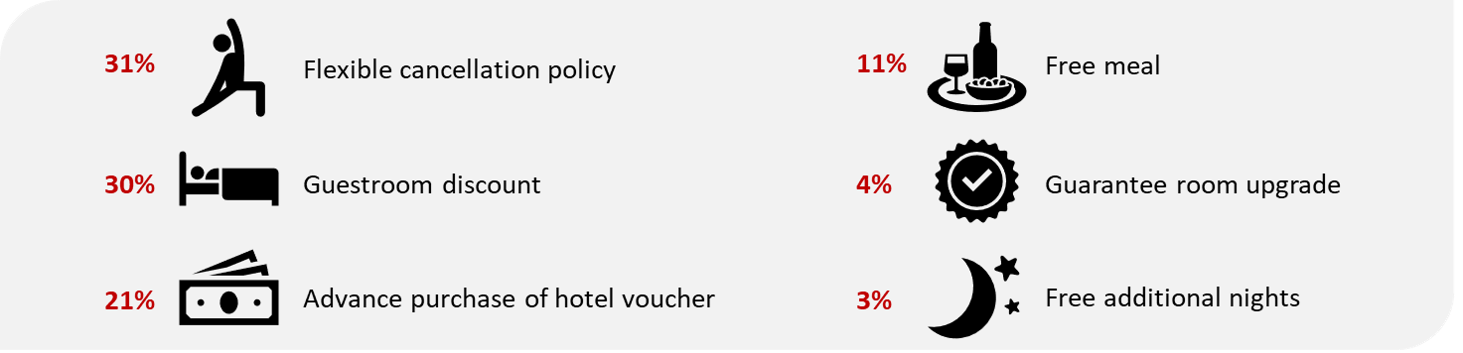

Discount and Promotion

What are the guestroom promotions or packages you are currently implementing?

Source: HVS

What is the range of discount of the following offers?

Source: HVS

Over 60% of responses are giving 20% to more than 25% discount on guestrooms. More than 50% of respondents are giving no discount on the spa. This could be attributed to the nature of its service with direct human interactions, as well as higher operating cost. Over 70% of respondents have not yet applied discounts for meeting space due to the expectation that MICE demand will recover at a slower pace. It is expected that there will be small social events or weddings held at the Drive-In destinations.

Demand Profile

Pre-COVID-19 Domestic Market Share

Source: HVS

Most of the hotels generally had a higher portion of domestic demand. Prior to COVID-19, about 70% of the hotels reported that domestic demand accounted for more than 60% of the total demand. Some hotels’ demand is 100% driven by domestic travellers. Almost 20% of the hotels in four markets (Chon Buri, Kanchanaburi, Trat, and Nakhon Ratchasima) reported having a share of 70% domestic and 30% international demand. Chon Buri, consisting of Pattaya and Si Racha, had the most diverse share of demand prior to COVID-19. Pattaya being an international destination driven by leisure demand relied more heavily on the international market. On the other hand, Si Racha, driven by local corporate demand, is more dependent on the domestic market. Other markets such as Kanchanaburi, Nakhon Ratchasima, and Prachuap Khiri Khan, including the tourist destinations such as Hua Hin, Pranburi, and Kui Buri, have traditionally been driven by domestic leisure demand. Due to international travel ban and government’s initiative to boost domestic travel, the demand was mostly driven by domestic travellers in Q2 2020.

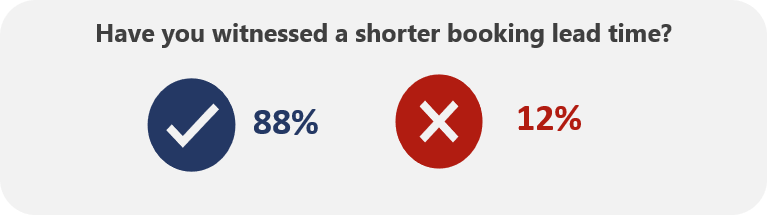

Booking Lead Time

Ranking of the largest to the smallest demand segment

Source: HVS

During the COVID-19 pandemic, hotels in the Drive-In Destinations rely heavily on the domestic market. The hotels witnessed the largest portion of domestic leisure and staycation, followed by corporate and MICE demand. Over 85% of the hotels observed a shorter booking lead time; 78% registered a lead time of less than one week and 17% registered lead times of 1-2 weeks.

Average Length of Stay

Average Length of Stay

Source: HVS

Over 95% of the leisure demand has an average length of stay of 1-2 nights, mainly attributed to weekends demand. About 65% of the staycation generally stays for at least two nights. 4% of the respondents said corporate demand stayed for more than four nights, due to long-stay demand in branded service apartments that was least affected by the COVID-19 situation.

Market Outlook

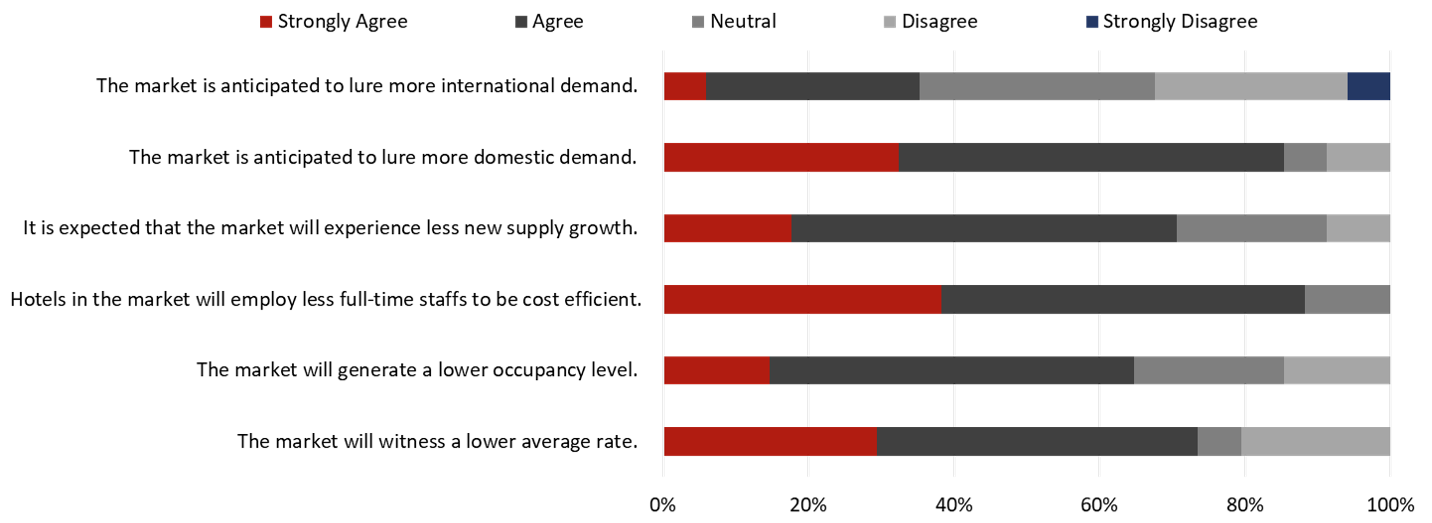

Assuming that the market will be recovered by Q2 2021, how would the market perform in comparison to the pre-Covid-19 period? Please rate how much you agree or disagree with the following statements.

Market Recovery

More than 85% agree that the market will lure more domestic demand and that the hotels will employ less full-time staffs to be cost-efficient. Only 35% agree that market will lure more international demand. Over 70% believe that the market will experience less supply growth. More than 65% are more pessimistic regarding the outlook of occupancy and average rate in the market.

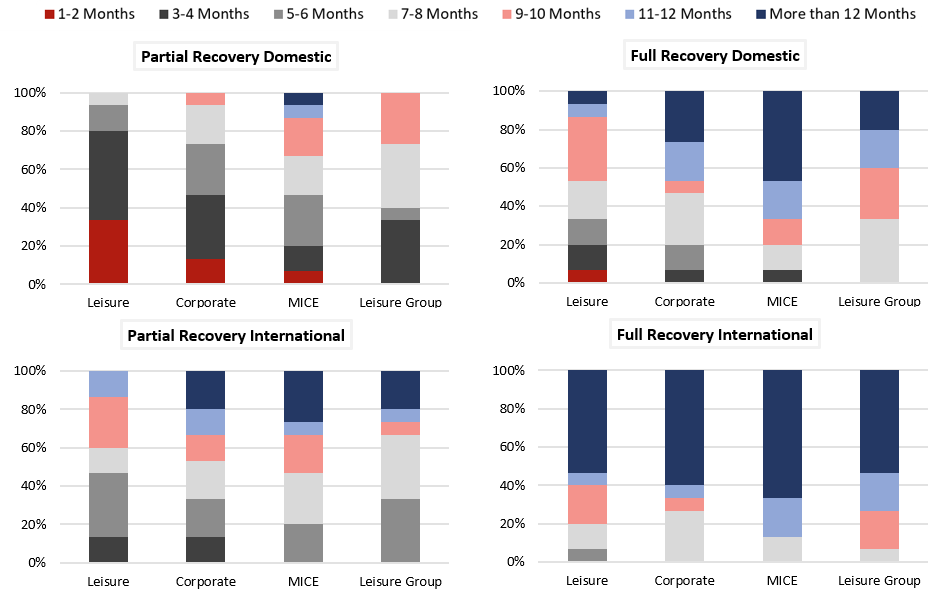

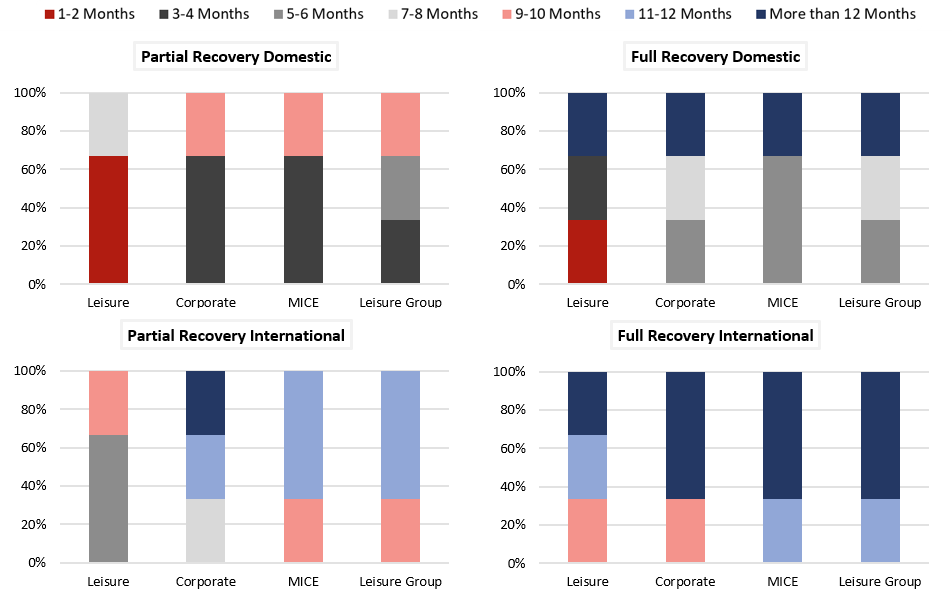

Market Outlook: Chon Buri (Pattaya, Si Racha, and Chon Buri)

How many months do you expect each market segmentation require to recover?

Source: HVS

Partial Recovery is defined as the market is 50% recovered. Full Recovery is defined as the market is 100% recovered. Being a short drive from Bangkok, 80% expects domestic leisure demand to recover between 1-4 months, while international demand can take up to a year.

Chon Buri: Estimated and Expected* Occupancy

Source: HVS

Due to the lockdown in Q2, 60% saw the occupancy drop to a range of 0%-15%. A gradual increase is expected in Q3 as the easing restriction begins to take place. By Q4, the occupancy is expected to hover between 60% and 75%. Market like Si Racha, which had a large portion of branded service apartments, was more resilient to the situation as it had a large portion of long-stay corporate demand.

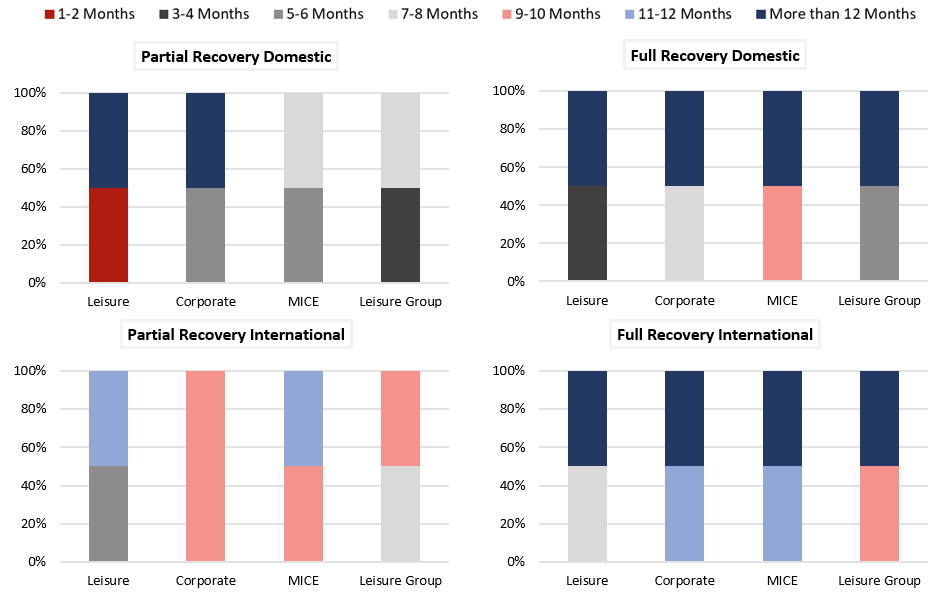

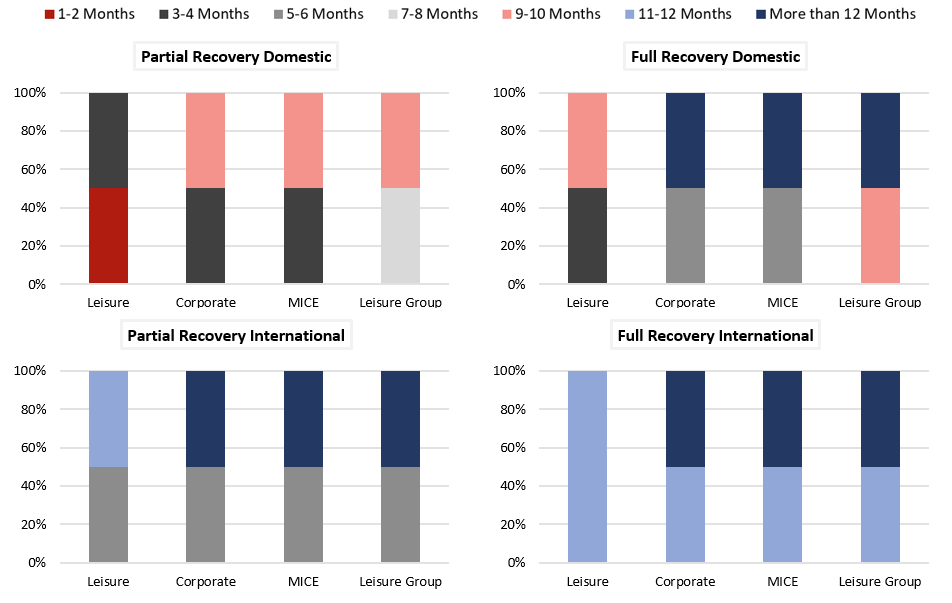

Market Outlook: Rayong

How many months do you expect each market segmentation require to recover?

Source: HVS

The sample size of Rayong market is relatively small because of the limited branded supply in the area. The mixed opinion is shown in the survey indicating a wide gap in each segment. Most hoteliers agree that it will take at least seven months to more than 12 months for the market to recover fully.

Rayong: Estimated and Expected* Occupancy

Source: HVS

Unlike the other markets in the survey, the hotels in Rayong did not record the occupancy level below 15% as none of them suspended their operations even during the lockdown. The optimistic outlook toward Q4 2020 is expected with occupancy ranging from 45% to over 75%.

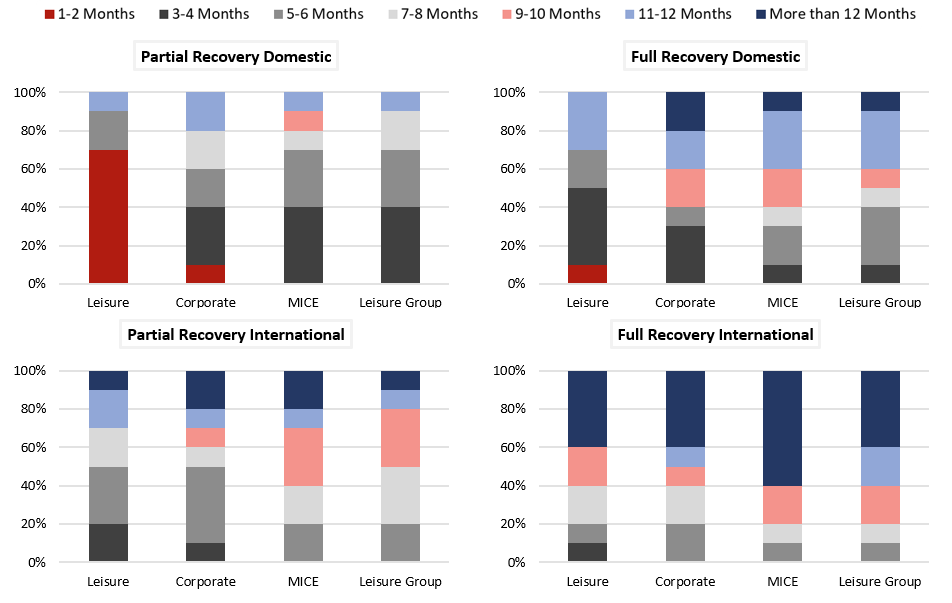

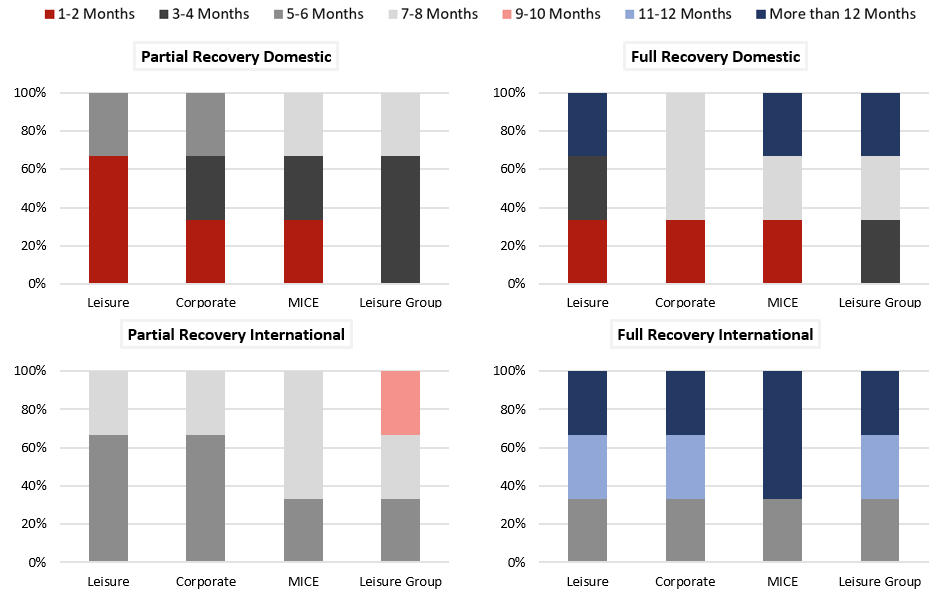

Market Outlook: Prachuap Khiri Khan (Hua Hin, Kui Buri, Pran Buri)

How many months do you expect each market segmentation require to recover?

Source: HVS

Prachuap Khiri Khan relies mainly on domestic demand. Therefore, it is expected that domestic demand will recover first, and it will take up to 12 months for international demand to recover as Prachuap Khiri Khan needs to compete with other leading destinations in Thailand such as Phuket, and Chiang Mai.

Prachuap Khiri Khan: Estimated and Expected* Occupancy

Source: HVS

Based on the survey result, most of the hoteliers in Prachuap Khiri Khan believe that the occupancy level will recover at a faster pace to approximately 30% to 60% after the ending of the lockdown in June.

Market Outlook: Nakhon Ratchasima (Khao Yai)

How many months do you expect each market segmentation require to recover?

Source: HVS

Same as Prachuap Khiri Khan, Nakhon Ratchasima is also mainly driven by domestic demand. It is expected that domestic leisure demand will recover first within a few months. The destination is also popular for Thai local companies’ incentive or outing trips. However, MICE and the corporate segment are expected to recover at a slower pace.

Nakhon Ratchasima: Estimated and Expected* Occupancy

Source: HVS

The occupancy level is expected to recover at a pace hovering around 45 to 75%. This could be attributed to its proximity to Bangkok with a number of golf courses. The high season can be observed in November and December when the weather gets cooler.

Market Outlook: Kanchanaburi

How many months do you expect each market segmentation require to recover?

Source: HVS

Due to the limited branded supply in Kanchanaburi, the sample size of the destination is relatively small. We observed a mixed opinion between each segment with a wider gap in each segment. The market is also driven by domestic demand; therefore, it is expected that domestic demand will recover faster than international demand.

Kanchanaburi: Estimated and Expected* Occupancy

Split opinion in expected occupancy level from June to September can be observed. However, it is looking very positive in Q4 2020 with an expected occupancy level of around 60% to more than 75%.

Market Outlook: Trat (Koh Chang, Koh Kood, Trat)

How many months do you expect each market segmentation require to recover?

Source: HVS

The hoteliers in the area had mixed opinions regarding the recovery and the occupancy outlook as there are significant differences in the clientele between the hotels on the islands and the hotels on the mainland.

Trat: Estimated and Expected* Occupancy

Being the most distant destination from Bangkok, together with a rather complicated logistic involving public transportation such as ferries, the occupancy is expected to be relatively softer, in comparison to other Drive-In Destinations, ending between 45% and 60% in Q4.

Final Thoughts

Drive-In Destinations: Estimated and Expected* Occupancy

Source: HVS

Most of the Drive-In Destinations markets were traditionally driven by domestic leisure demand, with the exception of Pattaya and Si Racha in Chon Buri that also captured a large portion of international and corporate demand. The situation of COVID-19 has emphasised the reliance on domestic demand in these markets. Around 65% of the hotels witnessed a drop in occupancy, particularly during April and May due to the nation-wide lockdown. As the easing of restrictions began on 1 June, all the markets are expecting a gradual increase in occupancy toward the latter half of the year. The hoteliers are more optimistic toward Q4, with more than 70% of the hotels expect to see the occupancy reaching at least 45% in November and December. These markets may enjoy the first-mover advantage when it comes to the recovery speed; however, it might only be a short-term gain, considering that once COVID-19 situation improves, a large portion of domestic demand may switch outbound. Additionally, as destinations, they will also have to compete with other prominent destinations in the country, such as Phuket, Chiang Mai, and Koh Samui. As the occupancy level recovers, the pressure will be put on the average rate. Owners are required to make prudent decisions in the short-term while adjusting their expectations towards a full recovery.

.jpg)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)