Interest Rate Trends & the Myth of “Normal”

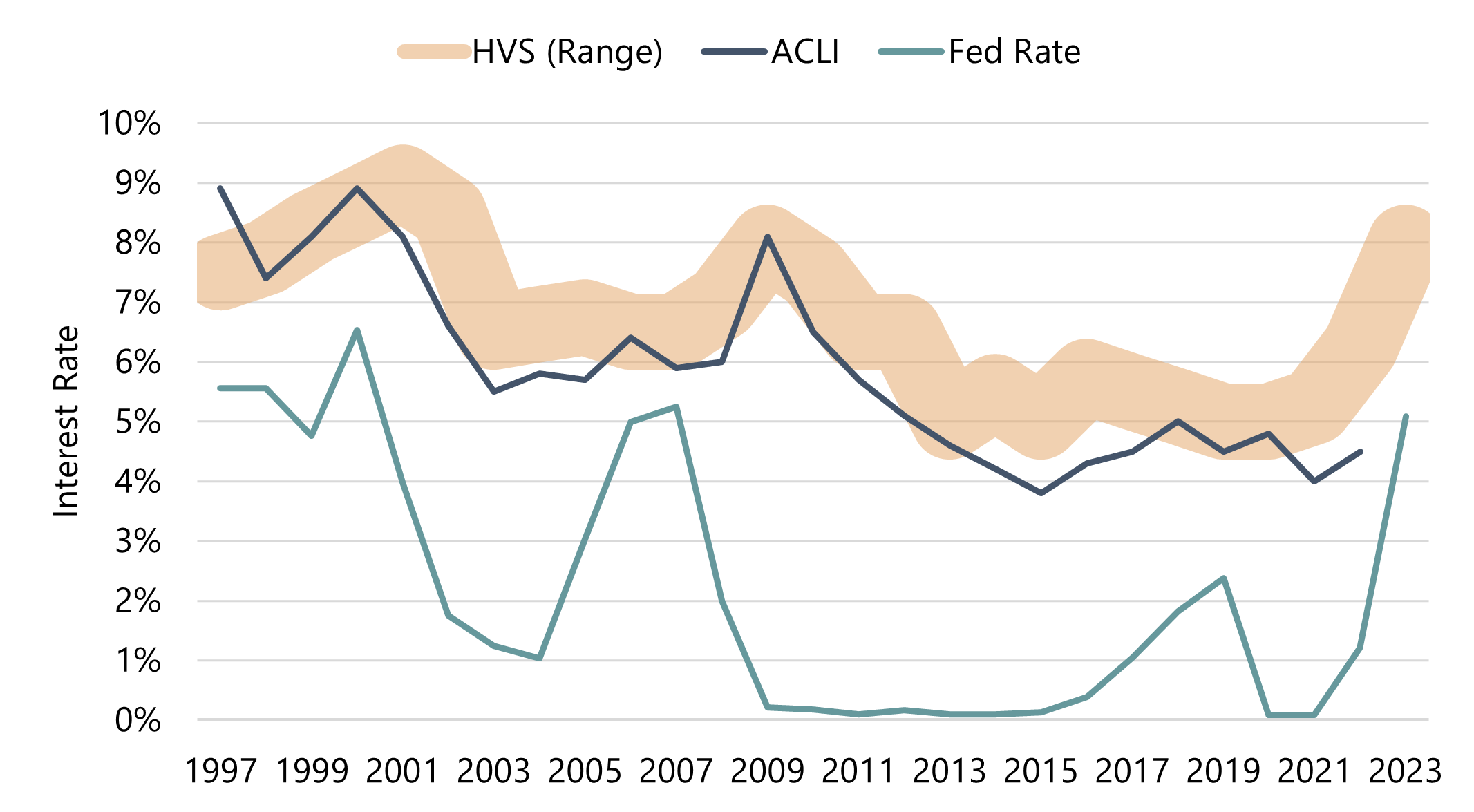

In order to determine reasonable expectations for debt pricing in coming years, HVS has reviewed publicly available data for actual hotel mortgages made by members of the American Council of Life Insurers (ACLI). This data primarily represents loans on higher value assets that would be considered credit-worthy by those companies. Additionally, HVS continually tracks hotel mortgage lending trends through conversations with active market participants and a review of actual hotel mortgage terms across a wider swath of the hotel financing landscape. This monitoring of the hotel mortgage market is routinely tracked, discussed internally, and updated multiple times per year. The following chart illustrates trends in interest rates from 1997 through the latest year of data, as tracked by HVS and published by the ACLI, as well as the fluctuations in the federal funds rate over the same period. The HVS trendline in the table below reflects a range of interest rates rather than specific data points.Hotel Mortgage Interest Rates Compared to the Federal Funds Rate

Based on those considerations and a review of the data presented above, it is readily apparent that the idea of a “normal” interest rate is a fallacy. Over time, the federal funds rate has fluctuated significantly in response to macroeconomic conditions, which are substantially influenced by major, often unforeseen, events. In the time period shown, these have included the 9/11 terrorist attack, the Great Recession, and the COVID-19 pandemic. While the fluctuation in hotel interest rates has been slightly less volatile, it has generally followed the trend line of the Fed rate and offers no clear indication of a period of normalcy.

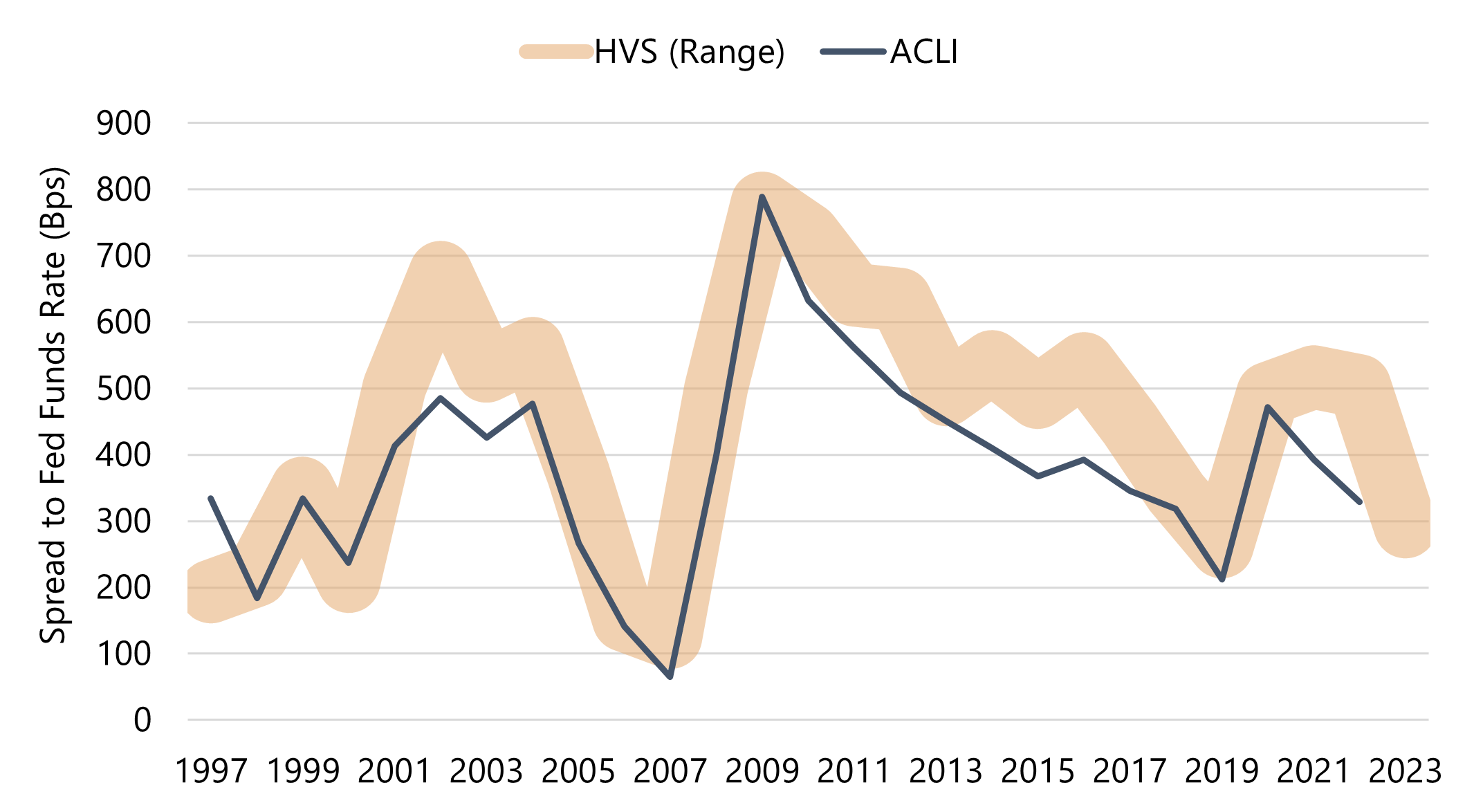

In addition to the comparison of rates presented above, it is also helpful to consider the spread of hotel interest rates in comparison to the Fed rate. The following chart illustrates the spread, in basis points, between the Fed rate and the hotel interest rates indicated by ACLI and HVS.

Spread Between Fed Rate and Hotel Interest Rates

Looking Ahead

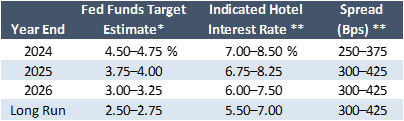

Fortunately, the FOMC offers forward-looking guidance on their targeted rate. As of March 20, when the last guidance was issued, the targeted “long-run” rate was 2.5–2.75%. This level represents the Fed’s estimate of a neutral funds rate that neither stimulates nor inhibits economic growth. As seen in the charts above, the Fed has not zeroed in on such a rate in recent memory, but instead has alternated between stimulating rates following a crisis and inhibiting rates when growth becomes too strong. Nevertheless, the Fed’s forward-looking rate guidance can provide some indication of where hotel interest rates may be headed if all goes as planned in coming years.In consideration of the historical trends presented above, we have estimated a range of potential hotel interest rates that correlate to the FMOC’s projected target rate in coming years, as of March 20. These projections indicate that if the Fed decreases the funds rate as planned, hotel interest rates are not likely to decline to the levels recorded from 2013 to 2021. Hotel investors needing to originate a loan in the near term should not be overly concerned about timing the interest rate market. On the other hand, for those with a low interest rate locked in through 2025, it may be worthwhile to wait as long as possible to obtain new financing. Of course, as the data presented in the first chart indicate, interest rates do not typically trend smoothly in the intended direction for very long. The choice to delay financing until interest rates are much lower may also mean choosing to face whatever macroeconomic crisis causes them to fall that far.