Prior to the onset of COVID, San Francisco was amid a tech-driven renaissance that placed the city and the nine-county San Francisco Bay Area as one of the top-growing metro areas over the last decade. Similar to during the internet-driven dot-com boom of the late 1990s, the city experienced tremendous economic growth, resulting in strong hotel performance. Market occupancy exceeded 80% between 2012 to 2019, while ADR increased at a compound annual growth rate of 7% for the nine years between 2010 and 2019.

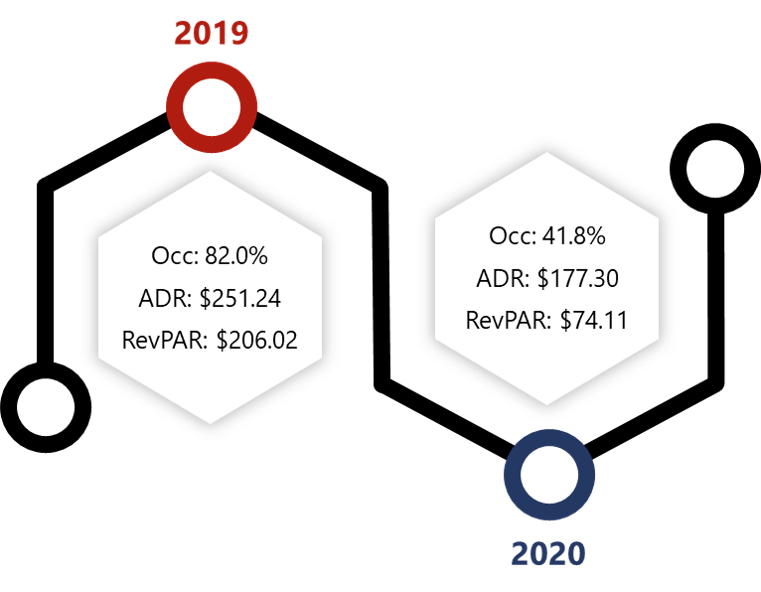

Prior to the onset of COVID, San Francisco was amid a tech-driven renaissance that placed the city and the nine-county San Francisco Bay Area as one of the top-growing metro areas over the last decade. Similar to during the internet-driven dot-com boom of the late 1990s, the city experienced tremendous economic growth, resulting in strong hotel performance. Market occupancy exceeded 80% between 2012 to 2019, while ADR increased at a compound annual growth rate of 7% for the nine years between 2010 and 2019.By many metrics, 2019 was a record year for San Francisco. According to the San Francisco Travel Association (SF Travel), the city broke visitation levels for the tenth consecutive year with a total of 26.2 million tourists. The Moscone Center had completed a $550-million renovation and expansion at the beginning of the year, supporting a record 1.2 million group room nights. In May 2018, Facebook had committed to the largest office lease ever signed in San Francisco, taking 755,900 square feet in the proposed Park Tower at 250 Howard Street. Visa and Pinterest also signed large leases in 2019, with Visa planning to move its headquarters from Foster City to a 13-story, 300,000-square-foot building in Mission Rock. In March 2019, Pinterest signed a 490,000-square-foot lease in a proposed office complex in SoMa. These positive trends resulted in a peak RevPAR of $206.02 for hotels in the San Francisco-San Mateo market.

However, going into 2020, there were already indications that demand in San Francisco was expected to soften in the near term. The 2020 booking pace for the Moscone Center at the end of December 2019 was roughly 850,000 definitive group room nights, far below the 1.2 million room nights accommodated in the previous year. A major factor in this decline was the relocation of Oracle’s OpenWorld conference to Las Vegas for the three years between 2020 and 2022. The fiscal impact of the move was estimated at roughly $64 million annually. Other factors influencing future demand in the city included McKesson’s relocation of its headquarters to Las Colinas, Texas, in April 2019. Charles Schwab also announced plans in November 2019 to move its headquarters to Denton, Texas, in January 2021, citing taxes and the high cost of doing business in the city.

2020 COVID Effects

The pandemic caused a swift upheaval in the city’s economic landscape. San Francisco was one of the first major cities in the United States to enact policies to curb the spread of COVID-19. In March 2020, San Francisco and five other Bay Area counties implemented a “shelter-in-place” order for all residents. The impact on hotels was tremendous, as the policy prohibited all non-essential business travel. In response, more than 70% of hotels in the city temporarily suspended operations because of the lack of demand. Hotels were finally allowed to reopen for tourism in September 2020; however, new regional policies enacted another ban on non-essential business travel in December 2020. By the end of the year, hotels in the San Francisco-San Mateo market averaged a RevPAR of $74.11 according to STR, a roughly 64% decline from peak 2019 levels.As San Francisco goes through this near-term “bust,” it is worth remembering that prior booms have always followed a recovery in this market, which explains why investors continue to pay top dollar for assets in San Francisco. Downturns provide opportunities for new businesses and investors to enter the market at reduced rents. During a low period, the San Francisco lodging market becomes more competitive with other gateway cities. This ebb and flow, boom and bust, is the natural pattern of the market. The San Francisco-San Mateo lodging market achieved 81% occupancy and $121 ADR at the peak of the dot-com era, only to experience a 40% RevPAR decline to the bottom of the bust in 2003. It took eight years for the market to recover to the prior RevPAR level, and then it blew past that performance with double-digit gains in ADR for five years, along with occupancies in excess of 80%. While it remains uncertain how this downturn will play out for San Francisco in the near term, including the exact timing of the course of the recovery, there is no doubt that the city will regain its vibrancy over the long term.

Other Implications

The impact of the pandemic has been unprecedented, with effects rippling throughout all sectors of the economy. Prior to the onset of COVID-19, the San Francisco Bay Area was seen as an unparalleled economic engine, primarily driven by the high-tech industry. However, companies such as Salesforce, Google, Apple, Twitter, and Facebook, which had previously supported strong growth with major office leases, are now offering some of the most flexible work policies. These high-tech firms have continued operations with a remote workforce, leaving urban cores such as Downtown San Francisco with empty offices, vacant storefronts, and quiet streets.By the Numbers

Source: STR

Source: STR

Source: CBRE

Source: CBRE

Source: JLL

Source: JLL

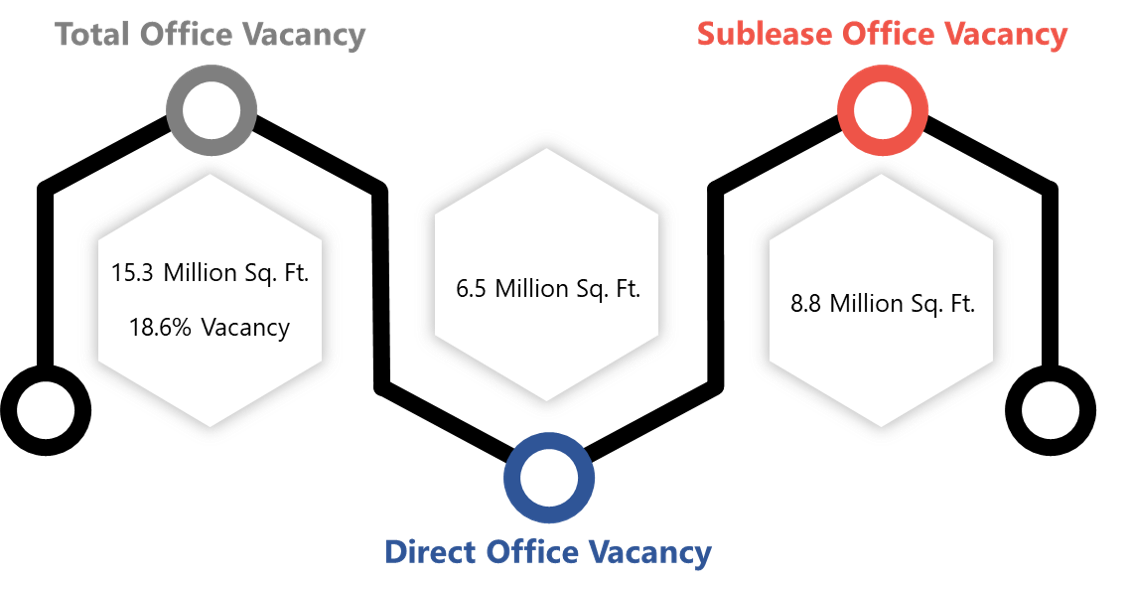

According to CBRE, overall office vacancy increased to 18.6% in February 2021, up from 16.9% in Q4 2020 and 5.4% in Q4 2019, with 8.8 million square feet of sublease space accounting for more than half of the 15.3 million square feet of vacant space available. Pinterest spent $90 million in August 2020 to terminate its 490,000-square-foot lease in SoMa that had been signed back in March 2019. In June 2020, Pacific Gas & Electric Company (PG&E) announced plans to vacate its 1.4-million-square-foot office complex in Downtown San Francisco, moving its headquarters to Oakland. Salesforce, the largest employer in San Francisco, listed approximately 225,000 square feet of space at 350 Mission Street for sublease in March 2021. At the same time, Salesforce canceled a separate deal for 325,000 square feet of office space at the forthcoming Transbay Parcel F mixed-use tower. While these trends appear bleak, we note that the vacancy rate in the Financial District increased from 1.8% in 1999 to 15.3% by 2002, during the dot-com bust, with rental rates declining by roughly 50%. Although economically painful, this upheaval created numerous opportunities for new firms and businesses to move into the city.

Though the near term will prove challenging, San Francisco will remain attractive as a business location given its urban infrastructure and educated workforce. The major companies supporting the local economy have indicated that they remain committed to the city, and investors continue to step into the market at record prices. Most recently, Kilroy Realty announced the pending sale of The Exchange on 16th. The four-building, 750,000-square-foot office complex is set to trade for $1.08 billion, or roughly $1,440 per square foot. Brokers have reported this as the highest price per square foot ever paid for an office building in San Francisco. One of the silver linings is that the pandemic has bolstered San Francisco’s already strong and growing life-sciences industry, with bio-tech firms stepping in to absorb some of the city’s sublease space. For example, Vir Biotechnology agreed in December 2020 to sublease roughly 134,000 square feet from Dropbox Inc. at its headquarters in Mission Bay.

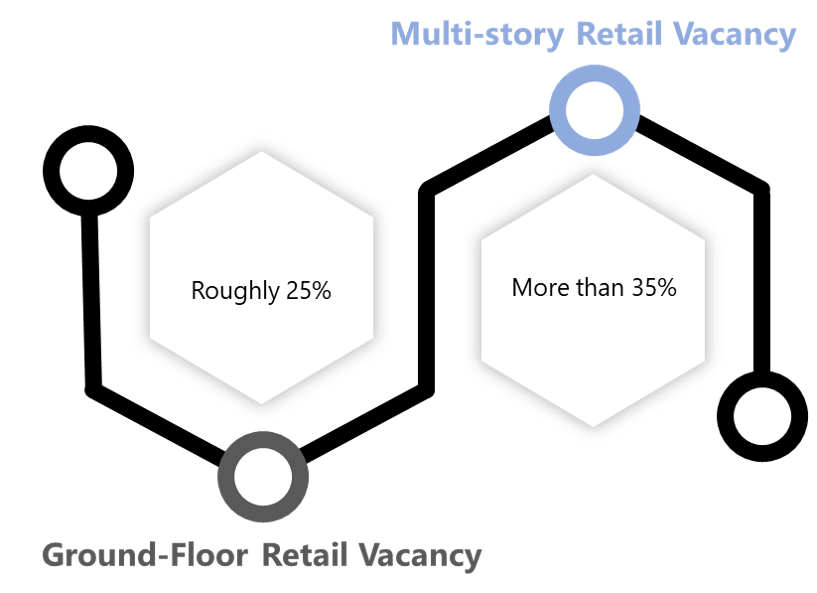

Union Square has been similarly affected, as the lack of tourists and office workers has resulted in numerous closures of restaurants and retail stores. According to JLL, roughly 25% of ground-floor retail space by square footage is vacant, while multi-story retail is more than 35% vacant. Major retail vacancies over the last several months include Gap’s Flagship at 870 Market Street, H&M’s West Coast Flagship at 150 Powell Street, Uniqlo at 111 Powell Street, and Marshalls at 760 Market Street. As retail reinvents itself throughout the world, the iconic Union Square market will also no doubt remain a desirable location and provide opportunities for new retailers to enter the San Francisco area. In September 2020, Ingka Group acquired the vacant 6X6 building at 945 Market Street with plans to redevelop it into a new retail destination anchored by the city’s first IKEA.

Looking Forward

After bottoming out in late March/early April 2020, RevPAR for the San Francisco-San Mateo major market experienced a slight recovery, peaking in August and September. RevPAR trended downward in Q4 2020, amplified by state restrictions in December/January prohibiting non-essential business travel. Lodging demand is projected to remain relatively flat through the first half of 2021, before a more notable recovery begins in the latter half of the year. The Moscone Center was recently converted to a COVID-19 vaccination site, and it remains unclear when larger gatherings will be permitted.Several hotels remain under construction in San Francisco, including the 195-room citizenM San Francisco Union Square, 236-room The LINE San Francisco, 248-room Kimpton Alton Hotel Fisherman’s Wharf, and 250-room SOMA Mission Bay Hotel. These hotels are tentatively scheduled to open sometime in 2021, but specific timelines remain uncertain given the ongoing pandemic. Recent or planned changes to existing supply include the 2020 rebrand of the Courtyard by Marriott in Downtown San Francisco to The Clancy Hotel, Autograph Collection; the 2020 conversion of the Loews Regency to the city’s second Four Seasons Hotel; the planned reflagging of the Park Central Hotel to the city’s second Hyatt Regency; and the planned renovation and rebranding of the Hotel Vitale to the 1 Hotel San Francisco. Given the city’s high barriers to entry, more than 6,000 rooms remain in the development pipeline.

While the near-term outlook remains relatively bleak, we are optimistic about the long-term economic strength of San Francisco and the greater Bay Area region. As U.S. residents become vaccinated and start to travel domestically, San Francisco will benefit from significant pent-up demand for travel. Given its proximity to world-class getaway destinations such as Lake Tahoe, Napa and Sonoma Valleys, and Monterey and Carmel, San Francisco serves as a major hub of leisure demand. Self-contained groups are expected to start returning to the city’s hotels in the fall of 2021, followed by a stronger recovery in meeting/group demand thereafter. Given uncertainties related to the pandemic, many conventions have been postponed or rescheduled. According to SF Travel, the Moscone Center is still showing a healthy booking pace for 2023 and 2025, with more than 650,000 definite room nights on the books.

Numerous technology companies have also announced the return of employees to offices beginning in July through the end of the year. While new remote-work policies will reduce the office population in the near term, as the market adjusts and sublease space becomes absorbed, commercial demand for hotel rooms is also expected to recover.

The last factor necessary to support a broad recovery is international travel, a major component of lodging demand for the greater San Francisco Bay Area. SF Travel does not expect international travel to rebound until 2025, indicating that the full recovery of the local lodging market will be prolonged. However, as in prior downturns, the city will remain attractive to hotel investors seeking to reap the rewards of a market poised for a strong recovery in future years.

We continue to actively consult in the San Francisco Bay Area and Northern California, which allows us to remain current with market trends. For more information, please contact our market specialists in the HVS San Francisco office: John Berean and Suzanne R. Mellen, MAI, CRE, FRICS, ISHC.

About John Berean

0 Comments

Success

It will be displayed once approved by an administrator.

Thank you.

Error