Pandemic-Era Travel Trends

Hawaii enacted some of the strictest travel measures in the United States in response to the COVID-19 pandemic. A mandatory two-week quarantine was enforced in March 2020 for all travelers arriving to the Hawaiian Islands; this quarantine applied not only to out-of-state visitors, but also to local interisland travel. As a result, a majority of hotels and resorts suspended operations. In October 2020, a Safe Travels program was introduced, easing the quarantine for inbound travelers contingent upon a negative COVID-19 test result within three days prior to arrival. This policy, in addition to the outdoor living and lifestyle of the islands, contributed to Hawaii being perceived as a safe haven from the pandemic.In the second quarter of 2021, occupancy levels began to notably improve concurrent with a strong rebound in domestic tourism. As most international destinations remained closed, U.S. travelers chose to visit domestic resort markets with a heavy focus on the outdoors and nature, such as Napa/Sonoma, Lake Tahoe, Sedona, Jackson Hole, and Hawaii. This spur in domestic travel supported a strong recovery in hotel occupancies, with demand rebounding to roughly 90% of pre-pandemic levels statewide.

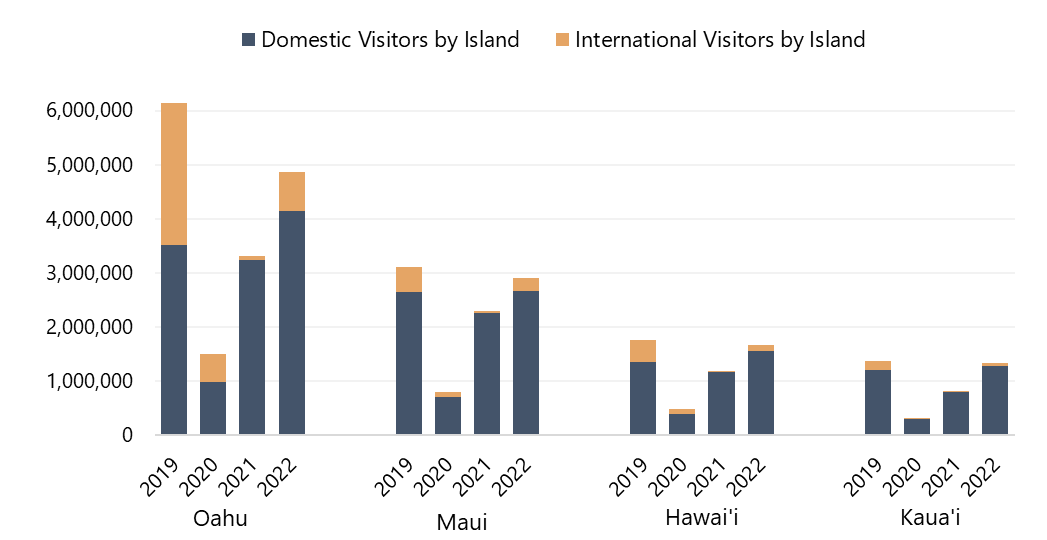

Visitor Arrivals by Island

Source: Hawaii Tourism Authority

Source: Hawaii Tourism Authority

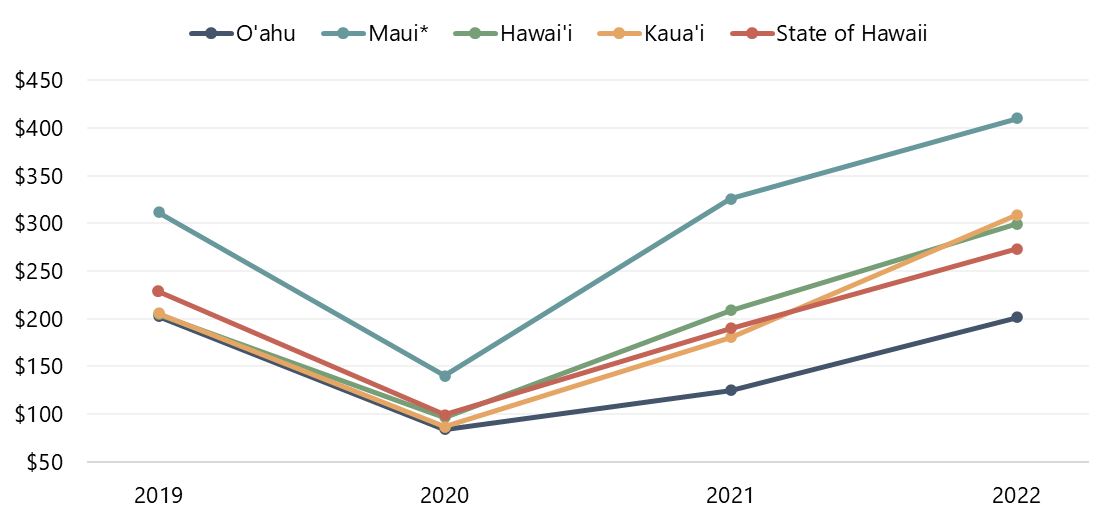

Average Rate and RevPAR Changes

The surge in “revenge travel,” or those making up for time lost during the pandemic, spurred phenomenal rate growth on the outer islands, particularly at luxury, resort-style properties. Conversely, many lodging facilities on Oʻahu were unable to capitalize on the rate gains achieved by the outer islands. This island’s slower rate growth can be attributed to several factors:

- The larger room inventory on Oʻahu and lack of room night compression

- Waikiki’s high-density, urban setting

-

The slow recovery of international tourism, which has historically generated up to 45% of visitation for the island

RevPAR Metrics by Island

*Includes the islands of Moloka’i and Lana’i

*Includes the islands of Moloka’i and Lana’i

Source: Hawaii Tourism Authority, Smith Travel Research (STR)

Source: Hawaii Tourism Authority, Smith Travel Research (STR)

Demand Outlook

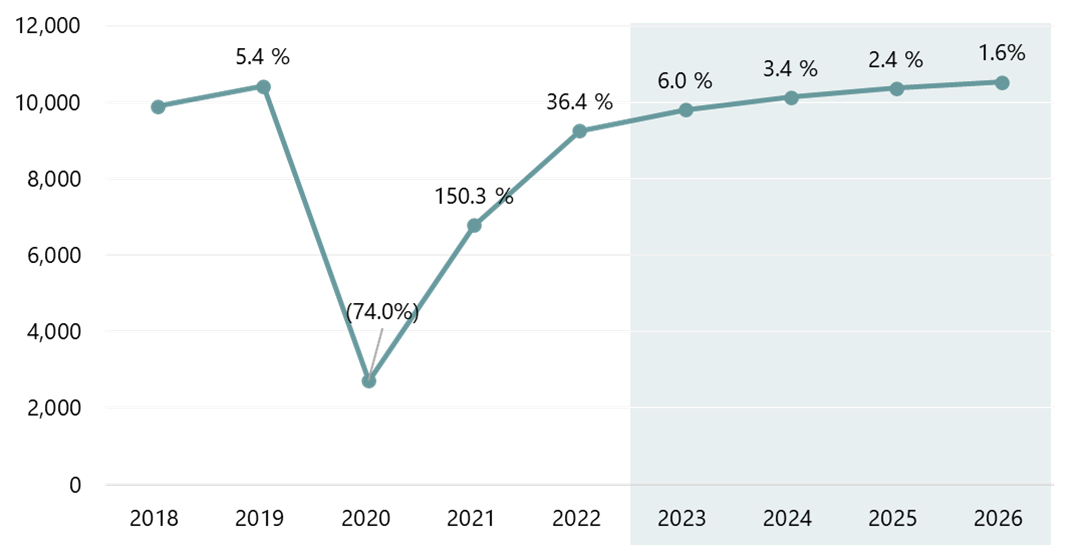

Going forward, demand levels are expected to continue to improve on Oʻahu, particularly as international tourism picks up. The Japanese market, having only produced roughly 300,000 arrivals in 2022, is expected to more than triple to about one million arrivals in 2023 based on the most recent Q1 2023 forecast provided by Hawaii’s Department of Business, Economic Development & Tourism (DBEDT). However, the return of this key market is likely to be more gradual in comparison to the surge in domestic tourism, particularly when considering the travel patterns of Japanese tourists and the cyclicality of the wholesale market. In addition, a weak yen, inflation, and high fuel surcharges on flights have also hampered the recovery of Japanese tourism. Golden Week, a multi-day national holiday in early May in Japan and one of the longest vacations of the year for many Japanese, is typically a major week for hotels and other businesses in Hawaii. Initial reports estimate that 2023 visitation levels during Golden Week were still down by nearly 50% compared to 2019 levels. Recent predictions from local hoteliers and other market participants anticipate a stronger rebound in Japanese travel in Q4 2023.Meanwhile, domestic travel is likely to soften as most international destinations have reopened and the U.S. dollar remains relatively strong. The lifting of COVID testing requirements prior to returning to the U.S. is also expected to support more outbound domestic travel. Following the significant rebound in 2022, demand levels are expected to gradually improve over the next several years, and DBEDT is projecting statewide visitation levels to surpass pre-pandemic levels by 2025/26.

Hawaii Tourism Forecast Q4 2022

Source: Hawaii DBEDT

Source: Hawaii DBEDT

Changes in Supply

Given the limited availability of land and high construction costs, Hawaii has one of the highest barriers to entry for development in the United States. However, the lodging landscape has experienced several notable changes since the pandemic, including the conversion of existing supply and the addition of new supply.Recent Openings

- The AC Hotel by Marriott Maui Wailea opened in May 2021 as the sister property to the adjacent Residence Inn by Marriott. This hotel marked the entrance of Marriott’s popular AC Hotels brand to the Hawaiian Islands.

- Dovetail + Co introduced the Wayfinder Waikiki (formerly known as the Waikiki Sand Villa Hotel) in December 2022 following a year-long renovation. The hotel’s coffee shop and retail store, B-Side, is currently open. The property’s remaining F&B outlets, including a tropical speakeasy and pool bar and the Redfish Waikiki (Foodland's poke restaurant concept), are expected to debut later in the year.

- Starwood Capital Group debuted the 1 Hotel Hanalei Bay (formerly known as the St. Regis Princeville) as its flagship property for the 1 Hotels brand in February 2023. The property is positioned to become the top luxury resort on the island of Kauaʻi.

- Sheraton Kona Resort & Spa at Keauhou Bay was rebranded in November 2021 as the Outrigger Kona Resort & Spa following its acquisition. The property reportedly began to undergo a $40-million renovation ($79,000 per room) in April 2023.

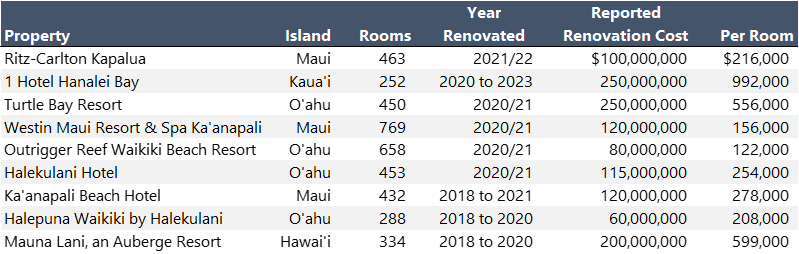

Major Renovations

Following the strong reception of the Surfjack Hotel & Swim Club and The Laylow, Autograph Collection affiliate, the emergence of design-forward, surf-themed boutique hotels has gained traction in Waikiki. Recent renovations have focused on a playful, modern design, which can be seen at several other popular hotels in Waikiki, including the Queen Kapiʻolani Hotel, Kaimana Beach Hotel, Wayfinder Waikiki, and White Sands Hotel.Recent High-Profile Renovations

Under Construction

- Kona Village is finally slated to reopen in July 2023 as a Rosewood Resort following a multi-year redevelopment. The property will primarily comprise standalone villas ranging from 1,000 to 6,200 square feet but will also feature several smaller oceanfront villas salvaged from the former resort.

- JL Capital is expected to debut the Renaissance Honolulu Hotel & Residences in late 2023. The 39-story, twin-tower property will be managed by Highgate Hotels and will feature 112 branded residences located above 187 hotel units.

- Continental Assets Management is in the process of redeveloping the former Remington College Building as a 104-room AC Hotel by Marriott; the property is planned to open in Q4 2024.

Hotel Transactions

Despite strong hotel performance in 2021 and 2022, transaction activity has remained somewhat muted over the last few years. Several notable transactions occurred on Maui in 2021, including record-breaking sales of the Residence Inn by Marriott and AC Hotel by Marriott in Wailea, as well as the Royal Lahaina Resort. In 2022, notable sales included the Maui Seaside Hotel, which is expected to be flagged under a soft brand following an extensive renovation and repositioning, as well as the Queen Kapiʻolani Hotel.While the current high cost of capital might deter some hotel investors on the mainland, the Hawaii market is poised for stronger transaction activity in 2023 and 2024 in light of the recent strong gains in RevPAR, especially as Asian markets reopen.

Conclusion

The Hawaii lodging market made a significant recovery in 2022, propelling many properties to achieve record-breaking RevPAR levels. While demand levels should continue to gradually improve over the next several years, operators will need to remain vigilant with revenue-management strategies to maintain the ADR gains achieved during the pandemic. With tourism levels projected to exceed pre-pandemic levels by 2025/26, the Hawaii lodging market should reach stabilization around 2025.Our team constantly monitors the Hawaii lodging market, and our many consulting engagements throughout the islands keep us abreast of the latest trends and shifts in the market. For more information, contact John Berean, who oversees HVS operations in Hawaii and Northern California.