Hotel Franchising in Europe is an update of our previous report published in 2019. This report aims to assist owners in increasing their understanding and awareness of the franchise business model and current market trends. The fees outlined in this report apply solely to hotels operating in Europe.

Introduction

Since our last edition of Hotel Franchising in Europe back in July 2019, the Hospitality Industry has gone through the most difficult time of its history. First, the COVID-19 pandemic, which emerged at the beginning of 2020, along with the resulting travel restrictions imposed by governments to reduce its spread and impact, have seriously tested the hospitality industry’s robustness, flexibility and adaptability. When demand started to recover by the summer of 2021, another wave of COVID-19 was followed in February 2022 by the Russian invasion of Ukraine. With the sanctions imposed by many European and American governments against Russia, important economic impacts challenged and continue to challenge the hospitality industry, from increases in energy and goods prices, disruptions to the global supply chain and difficulties in finding qualified personnel. The inflationary trends that first emerged during the pandemic have continued, becoming more significant.

These major events, coupled with the many acquisitions and mergers in the hotel industry over the past few years, have rapidly changed the landscape. The ‘big’ brands are now larger than ever and must continue to drive growth, lest they fall behind their peers. Their coverage, loyalty programmes and distribution channels are accordingly stronger than ever, but so is their bargaining power, which has been a strong force throughout the COVID-19 pandemic and continues to be post-pandemic. Technology continues to evolve at an incredibly fast pace. The OTA versus direct channel debate continues. Third-party operators have continued to grow and prove themselves as viable options. These are but a few of the factors that make a hotel owner’s choice of operating model essential for unlocking a property’s full potential and maximising its return. In order to help with this decision, this report will focus primarily on franchising and provide greater clarity on what terms can be expected.

Although franchising continues to be less prevalent in Europe compared to the USA, there is both anecdotal and quantitative evidence that it is gaining in popularity, both as a preferred means of expansion by the brands as well as an attractive model that allows owners to maintain a greater degree of control. Franchising is also important for brands entering new markets, as it allows them to increase their footprint more rapidly and rely on the owner or a local operator to manage the hotel; these local operators often already have a strong network of connections within their business community, local travel agents and tour companies, and so forth.

Hotel brands are arguably more important than ever, as they have a reach that independent hoteliers cannot match. For example, large operators have the resources to keep up with rapidly moving technology, whereas this might be more challenging for smaller independent hoteliers. Operators also have the depth of knowledge and the ability to send in their ‘specialists’ (be they in marketing, IT, operations, finance, or other areas) across the regions to assist their properties when needed.

When considering franchising, brand affiliation is important. The importance of selecting the appropriate brand for a hotel resides in the impact it will have on the hotel’s positioning within the market, its capacity to maximise occupancy and achieve room rate premiums, and the potential benefits of the chain’s distribution channels and know-how – and at what cost. All these factors will ultimately be reflected in the hotel’s bottom line, and therefore both owners and lenders will be interested in properly understanding and considering the overall benefits that a brand will bring to the hotel when assessing if the additional franchise cost is worth it.

Franchising in Europe

Franchising in Europe is not as transparent as it is in the USA where, because the Federal Trade Commission regulates the sale of franchises, information regarding each franchise fee structure is readily available. While discounts on the standard fees are often still offered, at least in the opening years, all parties know what the starting point is when they come to the table to negotiate. Because this report is focused on Europe, it is therefore limited to the information franchisors and franchisees we interviewed were willing to share as well as the information published in the hotel companies’ annual reports and other publicly available sources.

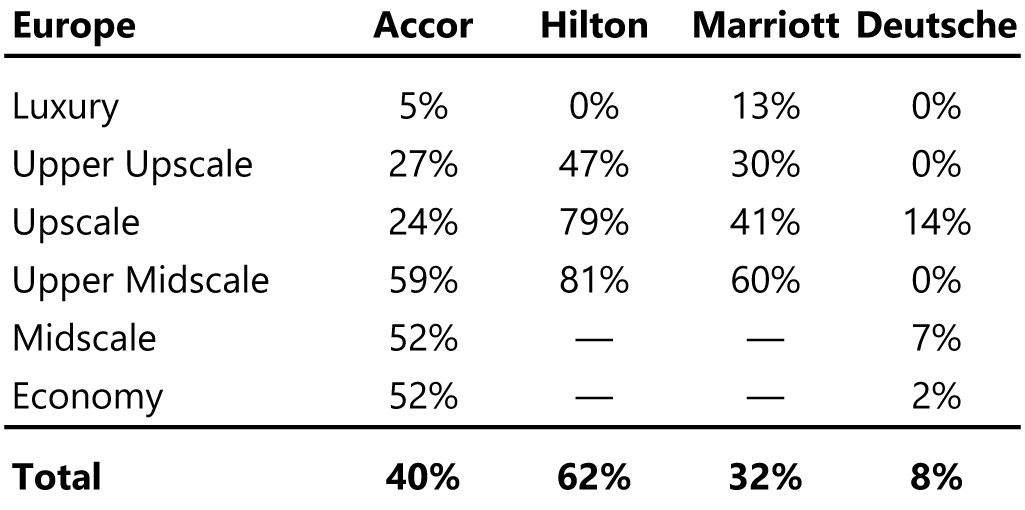

Table 1: Proportion of Franchised Properties in Each Market Segment

Source: Annual Reports, 2021

Although most European countries work closely together as a single trade zone, the region still exhibits a high degree of complexity and diversity. Unlike the USA, Europe has multiple languages, cultures, tourism dynamics, trade and franchise laws and so forth, so hotel brands must understand and comply with region-wide regulatory and disclosure requirements. As a result, franchise agreements in Europe experienced a slower uptake across the continent than on the other side of the Atlantic Ocean. Some countries such as Belgium, France and Italy have specific franchise laws that clearly specify what is required for contract outlines and commercial disclosure, while no specific obligations outside of the civil codes and the so-called ‘good practice’ are in place in other countries.

However, even though hotel brands and brand affiliations are experiencing remarkable growth in recognition around Europe, it is fair to say that challenges remain. For example, brands instantly recognisable and successful in one European country may have a more difficult time gaining recognition in other European markets. This is one of the reasons for many of the mergers and acquisitions in recent years; if a large international chain is able to acquire a local brand, it instantly gains significant coverage in that country or region and, as it is now under the umbrella of a large chain with greater brand awareness, it can more easily roll it out in other markets. For example, IHG has done this with the USA’s Kimpton, Jin Jiang has also done it with the Scandinavian Radisson and Marriott continues to roll out its Delta Hotels, the Canadian chain it acquired in 2015. On a larger scale, the acquisition of NH Hotels by Thailand’s Minor International provides an excellent example of how two chains with excellent regional coverage in separate parts of the world can combine to become a truly global hotel company virtually overnight. On this side of the COVID-19 pandemic, mergers and acquisitions have resumed with notable deals including Hyatt’s acquisition of the Apple Leisure Corporation, the merger of Accor and Ennismore, and Choice’s acquisition of Radisson Hotels Americas.

While hotels in Europe are still largely unbranded, there is clear evidence that this is changing. Brand affiliation in Europe is currently estimated at about 41% in 2022, up from around a third a decade ago. Despite this growth in affiliation, independent properties are still in the majority. Where franchising is concerned, this issue currently presents more opportunities than threats. In the USA, an estimated 70% of hotels are branded, which remains unchanged from three years ago. This clearly means that the opportunities for brand growth in Europe, including franchises, remain significant.

Whilst hotel chains are still reluctant to relinquish the control offered by management contracts for their more luxury brands, particularly in flagship locations, franchising is becoming a strong, often preferred means of expansion for midmarket and economy properties. This is clearly illustrated in Table 1, which looks at a few of the big brands as an example, where the operating model of each brand was disclosed in company SEC filings.

Franchisors in Europe

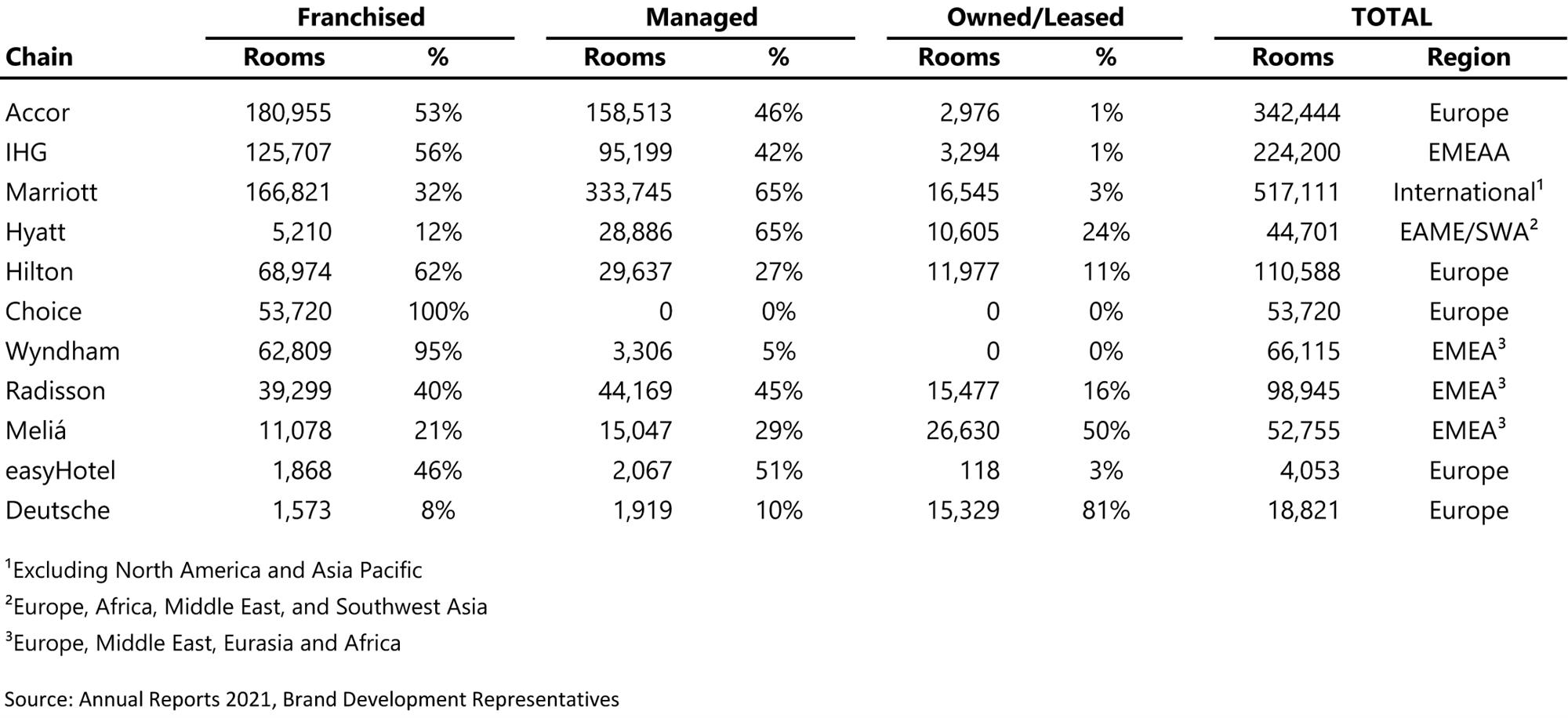

Our research included surveying a sample of hotel companies in Europe and reviewing annual reports and SEC filings for publicly traded chains operating in Europe. The sample spans the full spectrum from large international players to smaller European operators. Brands included in the sample range from economy limited-service to luxury full-service hotels. All of the companies sampled currently franchise some or all of brands in Europe or are planning to do so in the near future. Table 3 provides a list of the companies either surveyed and/or researched via their annual reports and other publicly available information. Table 2 shows the breakdown by operating model for a number of major hotel chains. Focusing on the biggest four chains in Europe, franchising clearly represents a significant portion of their European portfolios, with the franchised rooms accounting for approximately a third of Marriott’s portfolio (although, for disclosure complications, they report Europe, MEA and South America as aggregate, meaning the portion of franchised rooms specifically in Europe may differ), approximately half of Accor’s European portfolio, and the majority of IHG’s and Hilton’s European portfolios.

Table 2: Franchised Properties in Europe as of 31 December 2021

Source: Annual Reports 2021, Brand Development Representatives

Table 3: Chains Included in Research

Source: HVS Research

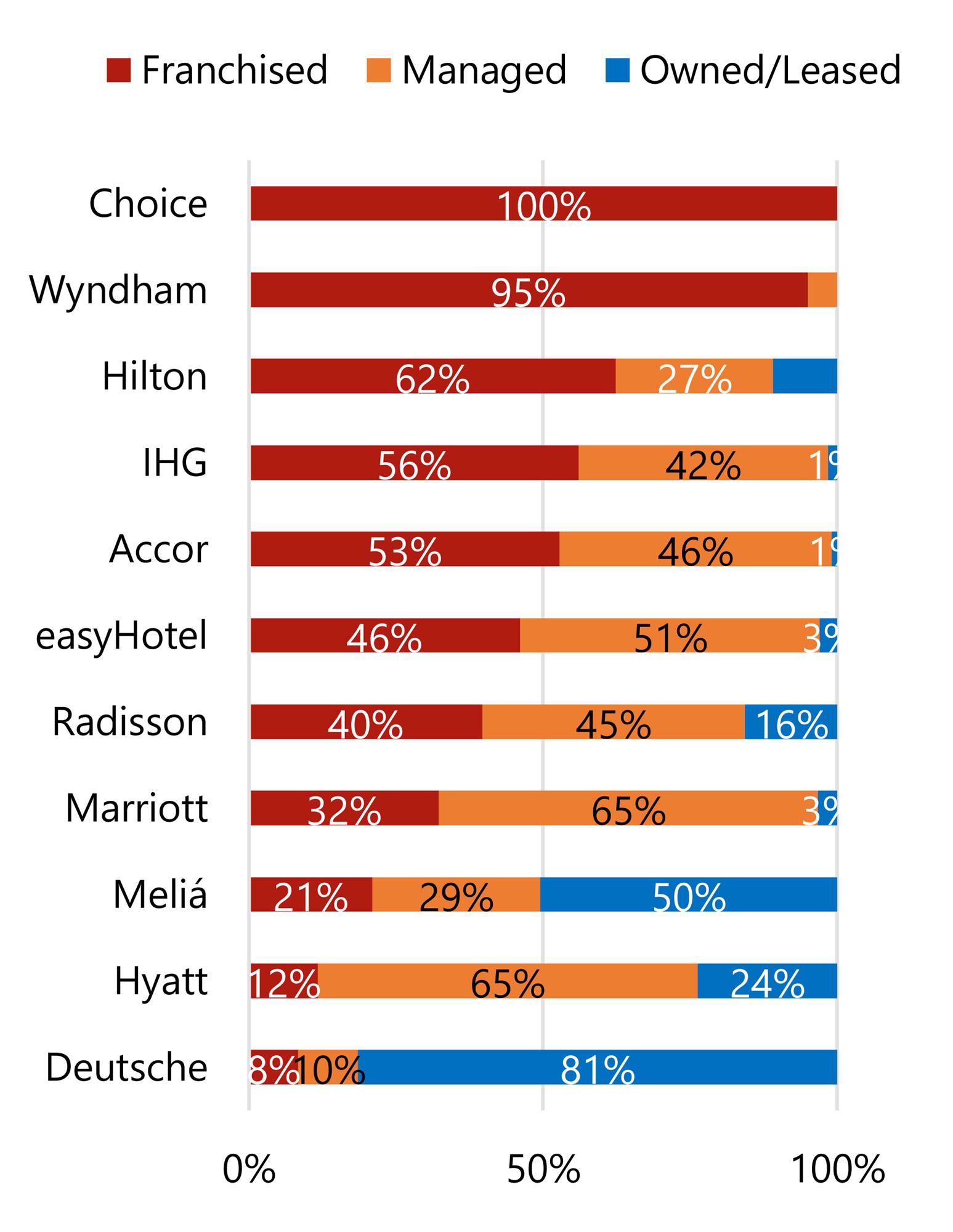

To highlight the increasing importance of this operating model, since the time of our 2019 report, the proportion of franchised properties has increased from 48% to 53% for Accor and a substantial increase from 51% to 62% for Hilton. Even companies such as Hyatt, which historically had no franchise presence in the region, now have several franchised properties in Europe (12%, or some 28 properties) and will continue to rely on this model to expand their limited service and extended stay brands. Table 4 provides an overview of the proportion of franchised hotels in Europe by chain.

Table 4: Proportion of Franchised Hotels in Hotel Chains

Source: Annual Reports 2021, Brand Representatives

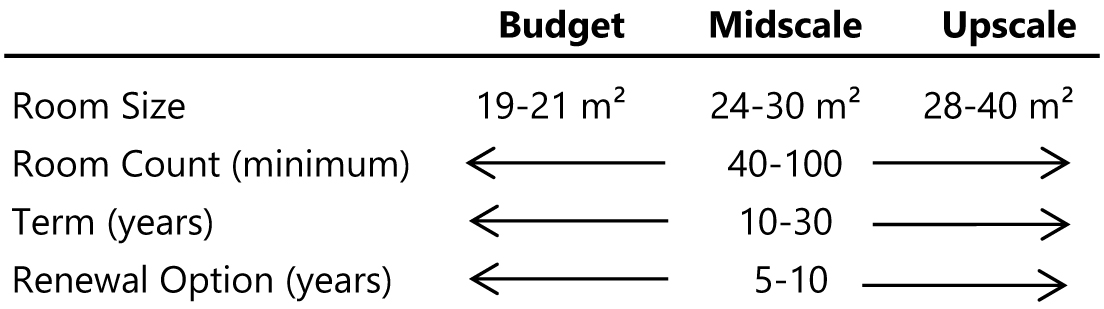

Basic Conditions

Table 5 sets out the general conditions required for building purposes and the terms for franchise agreements in Europe, by segment.

Table 5: Basic Conditions and Terms

Source: HVS Research

There is no set formula which defines what franchisors look for in a project. Typically, whether a property is an existing or new-build hotel is not an issue as long as the brand is a good fit for the type of product and the positioning of the hotel. Conversions are just as capable of achieving a profitable return as new builds. As with franchise fees, room requirements, term and renewal options are all open to negotiation. More desirable locations in strongly performing or strategic markets are likely to be offered more favourable terms, while the chains are likely to take into account what is considered the norm in the market when determining how strictly to adhere to required room sizes and other brand standards.

Lower-end hotel categories tend to offer more flexible terms while more upscale properties see larger minimum room counts and sizes and lengthier terms. A term of 20 years seems to be the sweet spot that most companies prefer, although many offer terms of 10 to 15 years, sometimes even less.

Franchise Fees

While there has been anecdotal evidence of hotel chains offering different fee structures, with both higher and lower levels of the various fees, we have not observed enough empirical evidence to suggest franchise agreement fees and fee structures have changed materially from pre-pandemic levels. The following section, therefore, remains broadly unchanged from our previous article.

Perhaps the most important part of evaluating the potential of a hotel franchise is the structure and amount of the franchise fees. A one-size-fits-all approach to franchising does not work in Europe, owing to the reasons discussed previously. Our findings are based on an average of ‘typical’ fee structures, which generally include the following:

Initial Fees

The initial fee typically takes the form of an amount based on the hotel’s room count. Research shows a wide range in initial fees, with average minimum fees of about €400 a room (the lowest fee at €150) and the average maximum of about €1,000 a room. Therefore, for a hypothetical 150-room hotel, this initial amount could range from as low as €22,500 up to €150,000, whereas for a smaller 75-room hotel, this amount would range between €11,250 and €75,000. In addition, some agreements call for a fixed or minimum initial fee to be paid as a lump sum upon submission of the franchise application; this is often the case for hotels with a lower room count.

The initial fee is typically paid (either partly or in full) upon submission of the franchise application and covers the franchisor’s cost of processing the application, reviewing the site, assessing market potential, evaluating the plans or existing layout, inspecting the property during construction, and providing services during the preopening or conversion phases. In the case of reflagging an existing property, the fee is often reduced and occasionally waived, as preopening advice and inspections are not required. Depending on the agreement, some franchisors will return the initial fee if the application is not approved, whereas others will keep a share in order to cover their administrative costs. If the fee was only partly paid on application, it is typically retained by the franchisor.

With that said, existing hotels will still be required to comply with the brand standards of the new franchise, which may require the purchase of soft goods, signage and even minor to possibly major refurbishment.

Continuing Fees

Payment of continuing franchise fees starts when the hotel assumes the franchise affiliation, and fees are usually paid monthly over the term of the agreement.

Royalty Fee

Almost all franchisors collect a royalty fee which represents compensation for the use of the brand’s trade name, services marks and associated logos, goodwill, and other franchise services. Royalty fees represent a major source of revenue for the franchisor. These fees are characteristically subject to negotiations between both parties, and can vary by brand, but typically range from 3.0% to 5.0% of room revenues. In some instances, franchisors require an additional percentage of other revenue streams, most commonly food and beverage revenue. In these cases, the average amount is 1% to 2% of total food and beverage revenue (or sometimes all non-rooms revenue), and this is payable on top of the room revenue in certain agreements. If included in the contract at all, F&B and non-rooms revenue fees are more often found in upscale and luxury brands than midscale and budget hotels.

Advertising or Marketing Contribution Fee

Brand-wide advertising and marketing consist of national or regional advertising in various types of media, including the Internet, the development and distribution of a brand directory, and marketing geared toward specific groups and segments. In many instances, the advertising or marketing contribution fee goes into a fund that is administered by the franchisor on behalf of all members of the brand. Franchisees ideally want their contribution to impact their location or region, which may not always be the case. From our discussions with various operators, these fees normally range from 2-4% of room revenue or 1-2% of total revenue. These fees typically vary by market and, in some instances, are paired with the reservation fee.

Reservation Fee

The fee and basis of calculation often depend on the source of booking for each reservation. The main sources are:

If the franchise brand has a reservation system, the reservation fee supports the cost of operating the central office, telephones, computers and reservations personnel. The reservation fee contains all distribution-related fees, including fees payable to third parties, such as travel agents and distributors. The calculation of this fee is the one that varies the most across our survey from one operator to another. The reservation fee can be based on a percentage of room revenue – a wide range of 1-5%, and even higher if based solely on the reservations generated by the brand’s distribution channels. It can also be calculated as an amount per available room per month (ranging from €4-10) or a combination of both approaches.

There does seem to be a movement towards the inclusion of the reservations fee in the advertising or marketing contribution fee or bundled into larger programme fees amongst some of the larger brands.

Frequent Traveller Programme Fee/Loyalty Fee

Franchisors often offer incentive programs that reward guests for frequent stays; these programs are designed to encourage loyalty to a brand. Many franchisors now require franchisees to bear their fair share of the costs associated with operating a frequent traveller programme. The cost of managing such programmes is financed by frequent traveller assessments. Frequent traveller programme assessments are typically based on a percentage (between 1.0% and 5.0%) of either rooms or total revenue generated by a programme member staying at a hotel. In some instances, a euro amount fee (say, €8) is payable to the franchisor based on the number of loyalty programme points awarded.

Miscellaneous Fees

Miscellaneous fees include fees payable to the franchisor or third-party suppliers for additional system and technical support and fees relating to training programmes and annual conferences. Sometimes franchisors offer additional services to franchisees including but not limited to consulting, purchasing assistance, computer equipment, equipment hire, on-site pre-opening assistance and marketing campaigns. The fees for these services are not generally quantified in the disclosure document. Our survey considers only mandatory and quantified costs.

Other – ‘All-In Fee’

Generally, these various fees are applied individually, but in some cases, franchisors combine a number of formulas which amount to an overall fee. These come in the form of an annual fee of a total euro amount which covers everything, or an overall percentage of total revenue.

Independent Management Companies

With the increasing presence of branded hotels across the world and many major chains focusing on franchising as the choice method of expansion, owners and brand companies are left with the challenge of ensuring their mutual interests are in capable hands. While many franchisees are owner-operators and have the management expertise to be successful, there remains a gap between owners that are unable or unwilling to control the daily operations of the hotel and the franchisors that provide the brand. This is where third-party operators (TPOs) have come into prominence.

Independent operators are an obvious choice for unbranded, independent properties, but can also be an excellent and valuable inclusion in franchised hotels. Owners may at first be hesitant to engage one, as it may seem like poor business sense to share the revenue and profit pie amongst three parties when it could be split between just two. When considering that the cost of operating under the brand is additional to these fees in the case of the independent operator, the nominal cost of the third-party operator may indeed be higher. That said, the fees charged often see a lower base fee in favour of a higher incentive fee. The brand gets its fees for bringing in the revenue, while the operator can focus on effective and efficient cost control and operation of the property.

Clearly, implementing a franchise agreement and a management agreement with an independent management company moves the hotel into the double fee scenario; however, we note that independent management fees are typically more competitive than those of the major brands. There are several other benefits including the following.

- Owing to their close relationships with franchisors, independent management companies are often able to help owners negotiate more competitive franchise fees;

- Cash flows are typically run at a tighter level with marketing costs (which are covered by the franchise agreement) usually lower;

- The term of the management agreement is characteristically much shorter (starting at a minimum lock-in of five to ten years) and exit options are typically more flexible.

The franchisor can also benefit from this scenario. In certain markets or for brands they prefer to franchise, it is preferable (and sometimes required) that they know and trust the operator, particularly for higher-end brands in their portfolios.

In conclusion, independent management companies open the door for expansion to both the franchisor and the owner.

Trends

Some of the main trends highlighted in our 2019 report have remained current throughout the pandemic and beyond, such as brands being creative in their fee structures. Indeed, in order to be competitive and demonstrate an alignment of interests with the owner, some brands only charge fees based on room revenues. Soft brands, which arguably are less identifiable to the typical guest as being associated with the larger chain, can go even further and may charge lower fees or use a different basis for calculating them. For example, a franchise agreement could have the royalty fee charged only on room revenue from bookings that have come through direct channels (albeit at a higher percentage than typical royalty fees) or from the brand’s central reservation system, similar to the treatment of reservation fees. As soft brands are often suitable for existing hotels that already have a strong name or history behind them, this provides some comfort to the owner that the agreement is fair and that they are not paying franchise fees on bookings they may have received regardless of the brand.

‘Choice, a prominent exclusively franchise brand, is increasingly offering more owner/operator-centric terms, like no reservation charges or contracts of a flexible duration.’

– Rustom Vickers, Head of Development at Choice Hotels EMEA

However, as a result of the pandemic, we have noted the emergence of new key trends. Customer confidence is one of them: many independent hoteliers have realised that in challenging times there are positives in having a brand affiliation, as savvy brands with solid platforms and established know-how can provide support packages and heightened levels of communication during difficult times. Over the last few years, large brands have been major components in negotiations with industry associations and local governments to provide support to their franchisees, and this is an important reason as to why many independent hoteliers made the switch to brands, particularly franchising, to be able to keep a form of control. Conversely, brands have aimed at cutting expenses through a shift to franchising, which required a less intensive level of support than managed hotels. Going forward, it is likely that this model will continue to be an attractive option for brand companies.

The trend of independent hotels joining soft brands may continue to accelerate as well. An increasingly popular model is ‘manchising’, a hybrid agreement whereby hotel owners engage a hotel operating company for an initial period, say three to five years, after which the contract transfers to a franchise contract. Another type of model is a short-term or flexible franchise contract, which is less frequent but occasionally used by brands for existing hotels that do not meet the brand requirements. For example, the hotel could become affiliated with the brand for say five years, undergo a property improvement programme (PIP) to meet the brand standards, say two years, and followed by a long-term franchise contract, say 15 years. These two operating models are becoming increasingly mainstream, and are expected to continue to attract independent hoteliers to brand their properties, probably often through franchising.

Overall, interest in franchising continues to grow. Owners in regions where franchising has been prevalent for some time have gained considerable experience of the model and a better understanding of what terms they can and cannot negotiate.

Conclusion

As discussed, a one-size-fits-all approach to franchise agreements is not possible in Europe owing to the independent nature of countries in the region, and even within the EU. Different countries impose different regulations and disclosure obligations, and hotel chains must be adept at understanding these as well as the expectations of local owners in order to remain competitive.

Clearly, franchise agreements have become more established in most markets across Europe and continue to gain in popularity and acceptance. The consolidation and acquisition of hotel chains have led to a sharp rise in the proportion of franchised properties in the portfolio of the top chains and, as they are now larger than ever, they will need to continue to rely on franchises to achieve the desired growth and remain ahead of their competition. Throughout the pandemic, brands have restructured to find cost efficiencies and, as franchising requires less support and infrastructure than managing properties, the region is seeing an increasing number of brands willing to franchise.

On the other side of the negotiating table, owners have more brands than ever to choose from. Although this increases the likelihood of finding a brand and chain that is a good fit for any one property, it also means that owners must truly do their research and understand the cost and commitment of their choices. With brands providing more extensive support to their franchisees over the last few years, independent hoteliers are increasingly more interested in branding their properties and many have already switched.

Taking on a franchise is a complicated investment. Selecting the appropriate franchise for the property entails exhaustive research and investigation. The information presented in this report provides some general insight into franchise fee structures that should only be relied upon as a preliminary resource.